Most of this text is directly borrowed from a Wikipedia entry about land value tax which I have edited for clarity. Although some of the text is mine, I make no claim to originality. -Jonathan Andreas

A land value tax (LVT) is a tax on the unimproved value of land that, unlike typical property taxes, disregards the value of buildings, personal property and other improvements.

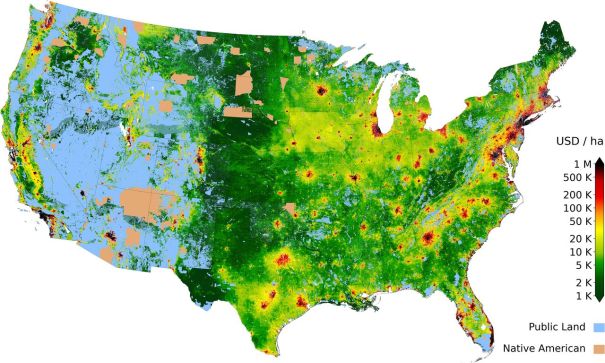

A land value tax would be highest in places where land valued more. This map estimates where private land is most valuable:

Interestingly, Iowa seems to have higher land value than surrounding states and there appears to be some very cheap land just a few miles east of Silicon Valley which is some of the most expensive land in the world. The main thing that makes land valuable is having more neighbors because higher population density means more customers, more jobs, and higher productivity per acre as shown in this map:

Although the economic efficiency of a LVT was known to Adam Smith,[1] it was most famously promoted by Henry George. In his best selling work Progress and Poverty (1879), George argued that when the site or location value of land was improved by public works, its economic rent was the most logical source of public revenue.[2] A LVT is also a progressive tax, in that more tax burden would fall on wealthy landowners than on the landless poor.[3] The philosophy that land rents extracted from nature should be captured by society and used to replace taxation is often known as Georgism.

Land value taxation is currently implemented throughout Denmark, Estonia, Russia, Hong Kong, and Taiwan. The tax has been applied in subregions of Australia (New South Wales), Mexico (Mexicali), and the United States (Pennsylvania). Singapore, and China have something similar to an LVT in that the government owns most of the land and leases it out, but the buildings on the land are owned separately as private property. This is equivalent to an LVT except that the “tax” is called a “rent” that is charged by the government. According to some Georgists, a land value tax should be considered a user fee instead of a tax, since it is related to the market value of socially created locational advantage, the privilege to exclude others from locations.

Economic effects

The value of land can be measured using two concepts:

- The sale price of land in fair exchange between an landowner who transfers ownership to a buyer. (This measurement is conditional on no LVT being applied, because when it does apply, the price is affected.)

- The land value of the site is also directly related to its demandable ground-rent, which is its potential for use in either production or residential capacities. The capitalization of this rent gives the land value too. Land which is not useful has no value.

Efficiency

Real estate bubbles

Real estate bubbles direct savings towards rent seeking activities rather than other investments, and can cause recessions (such as in 2008) which damage the entire economy. Advocates of the land tax claim that it reduces the speculative element in land pricing, thereby making the economy more stable and freeing up more money and attention to more productive capital investment.[17]

Because an optimal LVT would reduce land value to near zero, owners would only pay for the value of improvements like buildings which should not fluctuate much in value unlike the value of a location which fluctuates wildly.

Political challenges that prevent implementation of LVT

The point of an LVT is to reduce the value of land to zero. Since landowners possess significant political influence, this has been the main deterrent of the adoption of land value taxes.[18] In order to get an LVT, we’ll have to get the politically powerful to go along with it and they not only have a strong self-interest for opposing the LVT, but they also have some good ethical critiques.

Ethical critiques

The biggest opponents of LVT have always been wealthy landowners because they have tremendous political power and they have the most to lose. Richard Ely is an economist who supports the LVT and sympathizes with landowners. He argues that it wouldn’t be fair to penalize them simply for owning land. Two potential solutions would be to announce a change in policy now that will take place in 20 years so that markets have time to adjust gradually or to compensate landowners for their loss by paying them cash which they could reinvest in forms of capital that can be created like improvements to their land. Furthermore, landowners are already paying real estate taxes and for the median homeowner, the replacement of a real-estate tax with a LVT could be implemented so that there is zero change in total taxation. There would still be landowners who lose (owners of vacant lots) and landowners who would gain (owners of capital-intensive apartment buildings), but it could be implemented in a way that produces little change for most homeowners. Every policy change creates some losers somewhere, so

Ironically, Karl Marx opposed the LVT because he was worried that it would help to preserve capitalism by making capitalism work better. He was undoubtedly right about that.

Practical implementation challenges

There are several practical issues involved in the implementation of a land value tax. Most notably, it needs to be:

- Calculated fairly and accurately,

- High enough to raise sufficient revenue,

- But not too high causing land abandonment, and

- Billed to the correct person or business.

1. Assessments/Appraisals

In theory, levying a land value tax is straightforward, requiring only a valuation of the land and a register of the identities of the landholders. There is no need for the tax payers to deal with complicated forms or to give up personal information as with an income tax. Because land cannot be hidden, removed to a tax haven or concealed in an electronic data system,[19] the tax cannot be evaded.

Critics argue that precisely determining land value can be difficult in practice. Libertarian Murray Rothbard objected stating that no government can fairly assess value, which can only be determined by a free market.[21] However, this isn’t a major impediment because land-value appraisal techniques have dramatically improved since Rothbard’s day due to modern computerization and statistical techniques like multivariate regression analysis and geographic information system (GIS) in the 1960s and 1970s.[22] Firstly, free market businesses are already determining the value of land. For example, valuators in the home insurance industry are already performing such a function on a daily basis when, in order to calculate an insurance premium, the valuator must separate the value of the home from the indestructible value of the land beneath the home itself using market evidence from selling prices and rentals.

Secondly, governments are also already estimating the value of land as part of the process of assessing real estate taxes and the same process can be used to assess land value via the residual method: the value of the site is the total value of the property minus the depreciated value of buildings and other structures.

Even if land value were harder to estimate than the real estate value that we are currently taxing (which is dubious), it would be better to attempt the correct tax and estimate it with a little more error than to implement a worse tax with more accuracy. But compared to modern day real estate tax assessments, it is much easier to estimate the value of just the land because that involves fewer variables and has smoother gradients than the value of buildings and other improvements. This is due to greater variation of building style, quality and size. The quality of the land itself is much less variable.

Limited revenue

Some LVT supporters are utopians who hope to replace all taxation with this single tax, but a LVT alone would not raise enough revenues to maintain the government at its present size.[24] But a modern LVT could reduce other taxes and increase efficiency.

Land abandonment

Requires clear ownership

In some countries, LVT would be nearly impossible to implement because of lack of certainty regarding land titles and ownership. For instance a parcel of grazing land may be communally owned by the inhabitants of a nearby village and administered by the village elders. In these situations, the land in question would need to be vested in a trust or similar body for taxation purposes. This kind of cooperative-owned land is common practice in Latin America and parts of Asia where cooperatives could pay the tax.

If the government cannot accurately define ownership boundaries and ascertain the owners, it cannot know from whom to collect the tax. The phenomenon of lack of clear titles is found worldwide in developing countries[26] and is a focus of the work of Hernando de Soto. Many developing countries have poorly surveyed land boundaries and much land ownership that is not legally determined because of lack of registration which leads to economic inefficiency because there isn’t any incentive to invest in land improvements nor ability to borrow using land as collateral. Proponents of LVT argue that it will help produce clearer land ownership because elusive landlords would simply lose ownership of the land if taxes are not paid.[27]

Incentives

As a model of how Land Value Taxation affects incentives, take for example a vacant lot in the center of a vibrant and growing city. Any landowner that must pay a tax for such a lot will perceive holding it vacant as a financial liability instead of an investment that passively rises in value.

A LVT does not increase the purchasing price of land. Tax incidence rests completely upon landlords. This is to say that landlords can not collectively raise the overall market price of land as a result of the tax.

Buyers will not pay for the anticipated appreciation of land since such appreciation is taxed away. From the seller’s perspective, land costs more to continuously maintain ownership of. Thus, Land Value Taxation gives buyers of unused/underused parcels in central locations increased leverage over sellers who would use it productively.

Similarly, the selling price of anything that is fixed in supply will not increase if it is taxed. Since there is, for all intents and purposes, a fixed supply of land, a land value tax is paid by the land owner.

Furthermore, unlike taxing goods that carry higher purchasing prices as a result of higher production costs, land does not increase in price when taxed. This is because land simply exists. It is not produced by individual land owners.

For these same reasons, a land value tax is also not passed on to tenants as higher rent. Landlords are impelled to make land available to tenants as a means of generating the funds required to pay the Land Value Tax. Relatively speaking, landlords compete with other landlords for tenants instead of tenants competing with each other for space.

Land Value Taxation creates an impetus to either use a site for an income generating purpose, such as apartments, store fronts, office space, etc. or to sell part or all of the site. Of course, anyone who purchases the land will be faced with the same incentive, which is to use it or lose money.

The Land Value Tax paid per surface area is high in locations with high land values, especially cities. In vibrant cities, under use of land in the form of buildings which are underused, short, or even derelict are generally speaking converted to more intensive uses. Of course vacant or ground-level parking lots are also generally converted to building space and parking structures.

CC Photo by Flickr User Greg Wass

CC Photo by Flickr User Greg Wass

For example, the above image shows some of the vast vacant lots near my former home in Chicago with the Willis Tower (aka Sears Tower) in the background. This land has high value because of its location near the expensive condos and skyscrapers in the background, but it sits vacant because of speculators who are waiting for its value to rise and the property taxes are based more on the structures than on the land. If Chicago taxes were based upon land value rather than the structures, then the taxes on this land would be about the same as the taxes on the condominiums in the background. That would encourage the owners to sell it to someone who can make it productive rather than hoarding the land for speculation. The real estate tax on vacant lots it cheap compared with the condominiums and skyscrapers in the background because most of the property value that is taxed is in the high-rise buildings rather than in the land.

A LVT gives more incentive to use land rather than hoarding it for speculation. That would increase the supply of space for living, working, recreation, etc. Assuming constant demand, an increase in supply of constructed living space (a substitute for land), would decrease the rents for living space.

The LVT would replace taxes on buildings that are a large component of real estate tax. Taxes on buildings restrict the supply of building space. A revenue neutral shift from buildings to land increases the supply of building space.

Taxing land reduces the incentive for tax evasion. Multi-national corporations for instance cannot take land with them overseas. Land values are considered public information unlike income, sales, etc. GIS maps provide a means to easily compare taxes paid on land values. Such transparency reduces landowners’ ability to evade the tax.

Some ecological economists support the Georgist policy of LVT as a means of freeing or rewilding unused land and conserving nature by reducing urban sprawl. As Rick Rybeck wrote (PDF):

Transportation investments often increase nearby land values. This can choke off development, pushing new growth to cheaper sites remote from these investments. This “leapfrog” development creates a demand for infrastructure extension that starts the process over again. Transportation infrastructure, intended to facilitate development, thus chases it away. Resulting sprawl strains the transportation, fiscal, and environmental systems upon which communities rely. …[An LVT would reduce] the tax rate on assessed building values and increase the tax rate on assessed land values. The resulting compact development should facilitate better transportation and accommodate economic growth with reduced fiscal and environmental costs.

LVT is a more ecological tax because it discourages the waste of locations, a finite natural resource.[11][12][13]

Ethical arguments in favor of LVT

Religious scholars have claimed that land is a common gift to all of mankind.[28] For example, the Roman Catholic Church as part of its Universal destination of goods principle asserts:

Everyone knows that the Fathers of the Church laid down the duty of the rich toward the poor in no uncertain terms. As St. Ambrose put it: “You are not making a gift of what is yours to the poor man, but you are giving him back what is his. You have been appropriating things that are meant to be for the common use of everyone. The earth belongs to everyone, not to the rich.”[29]

—Pope Paul VI, Populorum Progressio (1967)

In addition, Catholic social teaching maintains that political authority has the right and duty to regulate, including the right to tax, the legitimate exercise of the right to ownership for the sake of the common good.[30]

From a secular point of view, land acquires a scarcity value owing to the competing needs of the community for living, working and leisure space. The unimproved value of land owes nothing to the individual efforts of the landowner and everything to the community at large. The primary secular ethical justification for LVT is that it is both more efficient and more equitable than alternatives.

Equity

A land value tax takes into account the effect on land value of location, or of improvements made to neighbouring land, such as proximity to roads, public works or a shopping complex. LVT is said to act as value capture tax.[32] A new public works project like a new park or subway station may make adjacent land go up considerably in value, and thus, with a tax on land values, the tax on adjacent land goes up. Thus, the new public improvements would be paid for by those most benefited by the new public improvements — those whose land value went up most.[33] Thus, a land value tax would tax wealth that is created by government, allowing a reduction in tax on privately created wealth.[34]

Additionally, a land value tax is also a progressive tax,[3][35] in that the tax burden is entirely based on land ownership, which is highly correlated to wealth,[36] and there is no means by which landlords can shift the tax burden onto tenants or laborers. Thus it would be paid for by those with a higher ability to pay, and reduce the tax burden of lower income families. Land value capture would reduce economic inequality, increase wages, remove incentives to misuse real estate, and reduce the vulnerability that economies face from property bubbles.[37]A

An LVT would reduce problems with gentrification

The problem of gentrification is that when a neighborhood becomes a more desirable place to live, the property values rise and rich people move in, displacing less-affluent long-term residents. The only two ways to combat this problem is to 1. prevent a neighborhood from becoming a nice place to live, or 2. to build more housing in nice places to make room for both affluent newcomers and the less-affluent long-term residents.

A land value tax would help reduce the problems of gentrification by hitting both issues. First, it makes elite neighborhoods less desirable by taxing away the benefits of living in areas with more amenities. In theory, all neighborhoods would be equally desirable for purchasers if an LVT were implemented optimally and all purchasers had the same preferences. The rents in more desirable buildings would still be higher than in less desirable buildings, so there would still be some gentrification, but it would be less due to the fact that speculators would no longer have any incentive to congregate in fashionable neighborhoods and try to reap the profits of driving up property values.

Secondly, an LVT encourages developers to build more housing because it incentivizes owners to get the maximum use out of their land rather than speculating on it, LVT reduces the cost of acquiring land for development, and LVT reduces the speculative risk that developers face. Bad zoning laws may be a bigger cause of problems that constrains the supply of housing, but an LVT would still help.

See also:

- Land economics.

- Wikipedia’s entry on Land Value Tax also contains a history of the concept and many more examples of implementation.

- Wikipedia’s entry on Georgism: LVT is almost synonymous with Georgism, but each Wikipedia entry has slightly different information. For example, the Georgism entry goes into more detail about proponents and opponents.

Leave a Comment