Josh Bivens has the scoop:

Dallas Federal Reserve Bank President Richard Fisher has a secret paper telling us how to fight inflation: stop progress in reducing unemployment so that nominal wages never grow fast enough to actually boost living standards (or, never grow fast enough to boost real wages).

Last week, Fisher argued that a so-far unpublished (i.e. secret) paper by his staff showed that “declines in the unemployment rate below 6.1 percent exert significantly higher wage pressures than if the rate is above 6.1 percent.”

In other words, Dallas Fed President Fisher is worried that wages will rise if the Fed allows unemployment to fall further. This shows the elitist priorities of some of the central planners who steer the US economy. The goal of monetary policy should be to increase real wages, not to decrease them. The Fed clearly wants the total national income (GDP) to rise, and if the Fed does not want wages to rise, then the only possible way to increase GDP is for the incomes of capital owners to rise.

That would be an increase in inequality that would hurt most Americans because only a tiny percent of Americans at the wealthiest end of the income distribution gets more income from owning stuff (capital) than from working (wages). Monetary policy and monetary ideology matters for the lives of ordinary Americans, but almost nobody cares about it outside of a few elites. That is a huge problem for ordinary Americans. If you care about unemployment and stagnant real wages, you should pay attention to Fed policy.

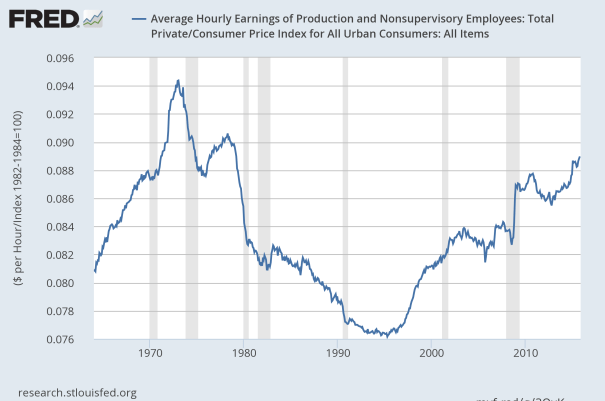

One of the great legacies of Alan Greenspan’s tenure at the Fed was that he kept doing expansionary monetary policy in the 1990s even when unemployment was already low because he didn’t believe that inflation was a problem. As a result, the 1990s saw the real wages of ordinary Americans begin a sustained rise and began to reverse the decline that started in the 1970s.

Anti-inflation mania is bad for real wages because wages don’t rise much unless unemployment is low and there is a short-run trade-off between lower inflation and lower unemployment. One way this works is that wages don’t rise if unemployment is high and that keeps prices (inflation) low because wages are 2/3 of the economy. If we never let unemployment get low, we reduce inflation in large part by keeping wages low. But this will increase inequality because higher GDP (income) has to go to someone and if it doesn’t go to workers, it must go to owners which includes all of the extremely wealthy people.

In the 1970s, the Fed changed its priorities from emphasizing low unemployment to emphasizing low inflation and ever since, wages have been relatively stagnant compared with the time from WWII until the 1970s when wages grew briskly. You can see the change in Fed policy by looking at the government’s own estimate of NAIRU, which is the amount of unemployment that the government thinks would be ideal because it could be achieved without causing inflation.

Before the mid 1970s, the Fed mostly kept the actual unemployment rate below the rate that the government thought was ideal and risked a bit more inflation which finally happened in the 1970s. Since then, the Fed has let unemployment get much higher than NAIRU, and has rarely let unemployment drop below it. That latter time period corresponds with declining or stagnant real wages relative to the earlier period when they grew robustly.

I’m not sure why the Fed changed course, but two things happened in the 1970s that may have contributed to their wage crushing policies. First was the monetarist intellectual revolution which emphasized low inflation more than low unemployment. The monetarists succeeded in shifting macroeconomic thought towards that priority.

Secondly, another intellectual revolution caused all the major economies to let their foreign exchange rates float in 1973 and let international markets determine currency values from then on. It seems normal now, but it was the first time this had happened. Gold had still been used for fixing foreign exchange values, so this was the end of the final vestiges of the gold standard. Letting exchange rates float created much more monetary flexibility than before when monetary policy was constrained by the desire to keep exchange rates stable and the Fed has used that additional flexibility to to keep wages and inflation low.