Jon Walker wrote a wonderful critique of Obamacare that Kevin Drum published in pieces so I’m copying it below so that it is all in one place.

1. State control combined with zero direct incentives for the states to make it work

The ACA left much of the regulation of the individual market and the implementation of the exchanges to the states, but it gave states no incentive to perform these tasks well. State/federal partnerships are common and there is nothing inherently wrong with them, but they almost always offer strong incentives for states to use good oversight. For example, with Medicaid, states are responsible for paying a portion of their costs, so they have a strong incentive to keep Medicaid costs low. The ACA should have given total control to the federal government or given states financial incentives for keeping premiums low, but lawmakers chose the worst of all policy designs. There was zero political justification for this design mistake.

2. Punishes low income people if their state or county tries to make the ACA work

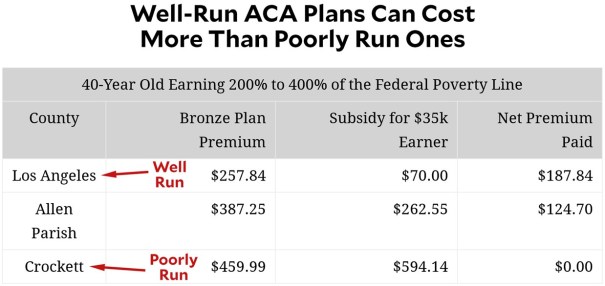

Even worse, the law actively punishes low-income people in states and counties which try to make the exchanges function well. ACA’s tax credits for the poor are based on the price of the second-lowest-cost silver plan, which means that regions with higher prices also provide higher subsidies. Perversely, it turns out that badly managed ACA plans produce premiums so high that the tax subsidies rise even higher—which produces a lower net cost for anyone who qualifies for subsidies. Conversely, in well-managed states like California, the net cost of a bronze or silver plan tends to be fairly steep.

3. Heavily encourages development of local monopolies

In any market there is already a strong incentive for companies to try to develop local monopolies, but the ACA design supercharges this with its subsidies based on the second-lowest-cost silver plan. The low-cost insurer in a market can game this design by offering two low-cost silver plans, thus making it nearly impossible for anyone else to compete. California adopted plan standardization rules to reduce this problem and make shopping for plans easier. The Obama administration could have adopted similar rules for Healthcare.gov but chose not to. This is often worst in rural places where there are concentrated hospital markets, making it impossible for any but the largest insurer to negotiate decent rates, or markets where the dominant hospital network is the insurer. Of course, once an insurer has created a monopoly position, it can then use it to create a potentially massive windfall. The ACA was premised on the idea that more insurance competition should be a top goal, but its design encourages the opposite.

4. Designed to get worse [less affordable] over time

The exchange plans and subsidies are based off actuarial value (AV). An actuarial value of 70% means the average person pays 30% of health care costs and the insurer pays 70%. The problem is that if health care costs rise faster than inflation, consumers end up paying the price. If health care spending averages $10,000 per person, cost sharing is $3,000. But if premiums go up to $20,000, then cost sharing goes up to $6,000. Even if you believe that the subsidy structure of the ACA was sufficient to make care “affordable” for people with specific income levels at the time of its passage, the design assures it will slowly make care unaffordable over time. What’s worse, ACA’s design includes a “failsafe” mechanism that will reduce subsidies if demand for insurance ever gets high enough—as it’s likely to do during a recession. Cutting help during a recession is a terrible policy move.

5. Accidently drove young, healthy people off the exchange

The ACA allows insurers to charge older people as much as three times more than young people pay in premiums; this is called a 3:1 age band. Compared to requiring insurers to charge everyone the same price, this added some real administrative complexity, but it was done to prevent premiums for older customers from getting too high. This inevitably means that premiums for younger people will be higher than they would be otherwise, but this at least was expected. What wasn’t expected is that young people might end up actually paying more for health insurance than older people. However, thanks to the subsidy design, it’s often the case that the net cost of insurance is more for the young than for the old. At the same time, if your income is high enough that you don’t qualify for subsidies, then it’s old people who pay more. This is a perfect example of people designing complex policies without even understanding how they work together. Regardless of whether you think the young or the old should pay more, it ought to be the same regardless of income level. …

6. Created a massive negative marginal tax rate

The ACA has a massive subsidy cliff, particularly for older people, which means if an individual earns a dollar over the subsidy threshold, they end up losing thousands. This cliff problem will only get worse as premiums continue to rise. Even without increasing overall spending it would have been possible to smooth out the subsidies to at least remove this massive negative marginal tax rate problem.

7. The creation and promotion of silver plans, when no one should buy middle level insurance

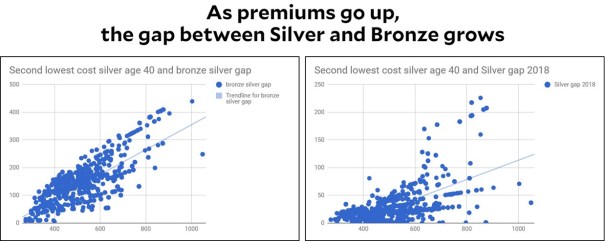

The ACA exchanges offer Bronze through Platinum plans, which makes Silver a middle-level option in terms of cost-sharing. The problem here is that most people have a pretty good idea of whether they’re likely to be high-cost or low-cost patients in a given year. Rationally, high-cost patients should choose Platinum plans and low-cost patients should choose Bronze plans, but the ACA subsidies are designed to force insurers to offer Silver plans—and they all but force many people to buy Silver plans. Most people should only be choosing the highest or lowest cost sharing option depending on their expected health, never the middle option.

Note that this problem gets worse the higher premiums go because the gap between Silver and Bronze also goes up. People who already pay the most are the ones who are hit hardest by the bias of the ACA toward pushing everyone toward Silver plans.

8. A needlessly complex mess of plans

In addition to the four metal tiers, the ACA requires plans to offer Cost Sharing Reductions to some lower income people but only if they buy Silver plans. These CSRs turn Silver plans into effective 94% AV, 87% AV, or 73% AV plans. That is seven different insurance tiers for every insurer, with numerous plans within each tier. It is a confusing administrative mess that also makes it difficult to explain to people why buying a Silver plan is way better than a Gold plan. These multiple subsidies could have been simplified, and these extra saving Silver plans could have just been merged with a “platinum” tier.

9. Terrible public data makes smart shopping impossible

The idea of the ACA was to bring down costs by getting individuals to be better, more conscientious consumers of their health care. This idea can’t even work in theory unless an individual has good data. However, the ACA has done a very poor job of providing people with the critical network data they need. Combined with the needlessly large variety of insurance plan designs, it is unreasonable to expect people to make the best choice.

10. Lets employers punish their sick employees

One part of the ACA allowed employers to charge employees significantly more if they don’t take part in “wellness programs.” These programs offer dubious value when it comes to improving health but have serious privacy and social justice issues. This effort, meant to help encourage sick people get healthy, has likely turned into a way for companies to discriminate against and financially punish those most in need.

Of course, another huge problem with Obamacare is that it doesn’t even achieve universal health insurance.

Most of the above problems could be avoided by repealing Obamacare and replacing it with Medicare for All. But the biggest problem with both Obamacare and Medicare is the biggest reason why American healthcare is so ridiculously expensive. The prices are just too damn high. Medicare for All would help reduce prices more than Obamacare, but it could go farther if we would follow these four ideas from Matt Yglesias that neither Republicans nor Democrats have touched:

1) Let in more immigrant doctors

American doctors earn substantially higher incomes than doctors in foreign countries, which means that foreign doctors could raise their incomes by moving to the United States. Conversely, American patients could save money by being treated by immigrant doctors.

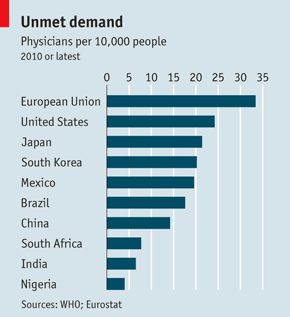

…despite high wages, the United States has a relatively small number of doctors per capita.

… foreign-born doctors face a great deal of difficulty in obtaining a license to practice medicine in the United States even as studies show that patient outcomes for Americans treated by immigrant doctors are just as good as those treated by native-born doctors. … Many foreign countries appear to have a comparative advantage in affordable medical education, and it would serve the interests of both the United States and those countries to have a clear pathway in place by which foreigners could be trained to work as doctors in the United States.

2) Curtail pharmaceutical monopolies [by funding prizes instead of awarding patents]

…Sarah Kliff recently wrote about a Hepatitis C treatment that costs $1,000 per pill. And yet [these] pills are not expensive to manufacture. Costly medications are expensive primarily by design. …the United States Congress has seen fit to create financial incentives for medical innovation by granting pharmaceutical companies monopolies known as patents that shield new drugs from market competition for years.

This leads to …windfall profits for drug companies. Those profits become the financial engine that makes new research worthwhile.

But patents also make innovation harder in some respects by making it more costly for new researchers to build on previous work. What’s more, they are hardly the only possible means of financing new research. Economists ranging from George Mason University’s Alex Tabarrok to Joseph Stiglitz have proposed moving away from medical patents to taxpayer financed prizes for key breakthroughs.

A large cash prize creates an incentive to innovate just as much as a patent does, but offers several important advantages. First, nobody needs to be priced out. All those $1000 hepatitis pills generate a lot of revenue, but also a lot of patients who end up with no pills at all. With a prize, the money is raised in a way that doesn’t need to exclude anyone. Prizes can also direct R&D efforts at problems that are genuinely important, rather than ones that happen to interest a large market. The patent system is better at generating treatments for conditions that annoy rich people (baldness) than conditions that kill poor people (malaria).

Last but by no means least, a prize-based system would reduce the amount of money and effort firms currently spend on trying to game the patent system. Right now, for example, companies like AstraZeneca spend time doing things like reformulating the active ingredient from Prilosec into a quasi-new drug called Nexium in order to get a new high-margin product to sell. Prizes could be targeted at innovations with real health benefits, rather than …payoffs for hacking patent law.

3) Let non-doctors treat patients

In some states, licensed nurse-practitioners are allowed to provide basic medical treatment within their sphere of competency without oversight from a doctor. In [most states] this is illegal. But the state-to-state variation allows us to compare the quality of care provided by NPs to that provided by MDs, and it shows that NPs are just as good on objective outcome measures, and better on subjective accounts of patient satisfaction.

If [all] states acted in line with Institute of Medicine recommendations and let their NPs practice autonomously, patients could get the cheaper health care they provide. Studies of Certified Nurse Midwives and Certified Registered Nurse Anesthesiologists have, …found that they treat patients as well or better than physicians.

These various categories of advanced practice nurses receive training and education that is not as time-consuming and expensive as the training provided to doctors. Consequently, their services — where legal — can be obtained more cheaply than those of doctors. Relying more heavily on advanced practice nurses would save money directly through this channel. It would also leave doctors with more time on their hands to treat patients who really do need to see a doctor, bringing more supply and lower prices to those cases.

A similar dynamic obtains in the field of dentistry. Most years the vast majority of people need no dental care beyond basic tooth cleaning that a dental hygienist can provide. But in many states it is illegal for a hygienist to practice without the direct supervision of a dentist [who have monopoly power over hygienists to raise prices and get a healthy cut out of hygienist fees for] routine tooth cleaning…

4) All-payer rate setting

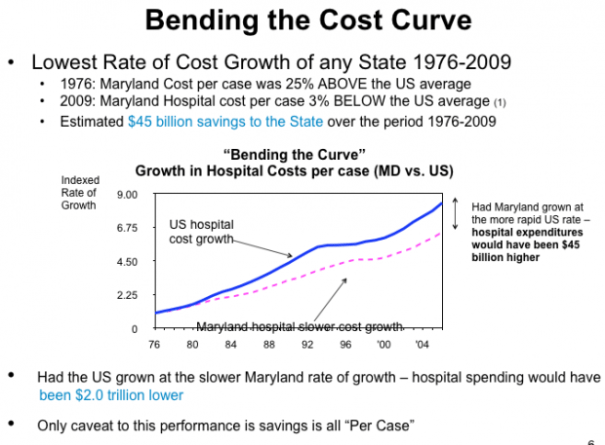

In [most countries with universal healthcare such as] Germany, the Netherlands, and the exotic foreign land known as Maryland they practice what’s called all-payer rate setting. That means that instead of each insurance company negotiating separately with each hospital group on prices, a government commission sets a price that everyone pays. And it works. Maryland has curtailed cost growth without inducing any noteworthy shortages of health care facilities:

Another advantage to all-payer rate setting beyond the simple ability to set low rates is that it would eliminate some of the necessity of doing everything through an insurance company middleman. Right now, one of the services your health insurer provides is a real insurance function that helps you hedge against risk. But for many people, the insurer’s most important practical role is as a [price] negotiator. Since the insurance company has a lot of scale, it can get a good price from a doctor or a hospital. An uninsured person would have to pay at a much higher rate.

[Eliminating] the insurance company’s role as a negotiator would [reduce administrative costs and] let insurers focus more on the insurance function… And by eliminating some of the advantages to sheer scale on the insurance side, it could also promote more competition in the health insurance industry.

Medicare for All is essentially a more extreme version of all-payer rate setting because Medicare would set the same rates for all payers. Ezra Klein wrote about a much less radical way to bring prices down by capping the maximum prices at a higher level than a typical all-payer rate. This would be much less radical than either Medicare for All or even all-payer rate setting.

Explaining why Americans pay so much more for health care than anyone else is really quite easy: Americans are charged higher prices for health care than anyone else [in the world].

Here are 15 charts proving the point… Cruelly, the uninsured are often charged the highest prices, because if you’re too poor to afford insurance, you’re also too poor to fight back against price gouging…. None of this makes even a little bit of sense. But Medicare could help fix it.

…In Health Affairs, Jonathan Skinner, Elliot Fisher and James Weinstein note data from Castlight Health showing that the price tag on one particular cholesterol test can range from $15 to $343 — and that’s just within the city of Dallas, Texas…

these prices are rarely, if ever, published, and often they’re not even the actual price people pay. If markets are going to work well, both buyers and sellers need a lot of information about how much things cost and how good they are. In health care, buyers are denied basically all of that information, and they’re occasionally unconscious when the transaction is being handled. This is not what a functioning market looks like.

But there are exceptions to America’s used-car dealership of a health-care system. One of them is Medicare. The way Medicare works — which is the way the health systems in pretty much every other country work — is that it tells hospitals and doctors what it’s willing to pay for various services and then they decide whether to accept Medicare or reject it. It’s a take-it-or-leave-it offer. Almost all of them take it. More than 90 percent of doctors accepted new Medicare patients in 2012 — a higher number, even, than accepted new patients on private insurance. The result is that Medicare beneficiaries pay much lower, and much more predictable, prices than people with private insurance.

… Skinner, Fisher, and Weinstein… suggest a simpler solution: why not cap all prices at 125 percent what Medicare pays?

The federal Medicare program has in place a complete system of prices for every procedure and treatment. It’s not perfect, but it is uniform across regions, with a cost-of-living adjustment that pays more in expensive cities and less in rural areas. If every patient and every insurance company always had the option of paying 125 percent of the Medicare price for any service, we would effectively cap the worst of the price spikes. No longer would the tourist checked out at the ER for heat stroke be clobbered with a sky-high bill. Nor would the uninsured single mother be charged 10 times the best price for her child’s asthma care. This is not just another government regulation, but instead a protection plan that shields consumers from excessive market power.

…why not just give [the same prices Medicare pays] to private insurers, too?

Well, one answer [why private insurers should start out being billed 25% more] is that the entire health-care system is organized around being able to charge these high prices. If everyone switched to paying Medicare rates overnight, you would see a wave of hospitals closing and device manufacturers going bankrupt. The system can’t take that much change, that fast.

…This …brings the variation in prices down. This is a plan to help the people who end up getting truly gouged — it will mean an end, for instance, to uninsured patients being charged 300 percent of what Medicare pays for an appendectomy.

The health industry would freak out, of course, because once prices are capped at 125 percent of Medicare’s rates, they know it’s a small step …towards All Payer Rate Setting — which is, more or less, a way of merging the savings of single-payer system with a lot of private insurers.

Leave a Comment