Jordan Ellenberg’s book also points out that the Laffer curve is another example of non-linear thinking. The idea is so common today that it now seems obvious, but in the 1970s it was so novel to most people that they gave it a new name even though it was already a very old idea for economists. They named it after Arthur Laffer who helped found a political movement known as supply-side economics based largely on this idea. Supply-side economics never developed much following among academic economists,* but it soon became a dominant economic ideology in the Republican party and as a result, Ronald Reagan reduced the top income tax rate from 70% down to 28%. 70% seems like a politically impossible rate given that Obama faced tremendous opposition against raising the top rate from 35% to 39.6% in 2013, but it had been 70% without much controversy through the 1960s and 1970s and it had been 90% or higher during the 1940s and 1950s.

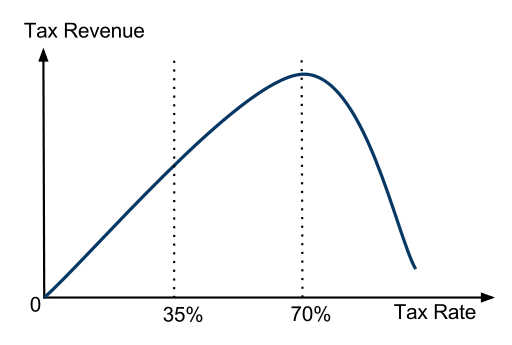

Although many textbooks draw the Laffer curve as peaking at around a 50% tax rate, that is probably just because the half-circle curve looks prettier than a more realistic curve like the one below which is based upon research by Trabandt and Uhlig (2011). Even this is a somewhat rough approximation, but it is about as good as we have at this point.

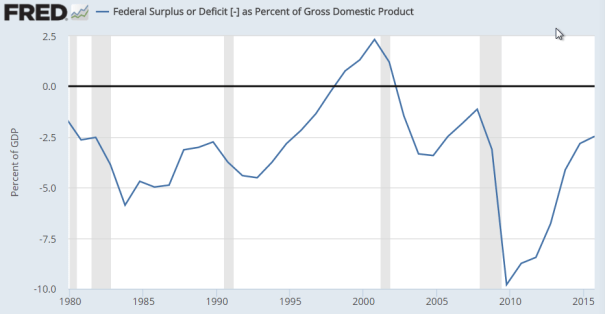

Unfortunately, many supply-side politicans haven’t paid much attention to their own theory and act like cuts in income taxes will always INCREASE tax revenues! They have fallen into linear thinking, but flipped the ordinary logic. In reality, despite Laffer’s claims to the contrary, the Reagan tax cuts caused a large increase in deficits in the early 1980s and the Clinton tax increases caused a large decrease in the deficit in the mid 1990s and then the Bush tax cuts caused the deficit to balloon again in the 2000s.

The Laffer-curve intellectual revolution largely explains why a 39% top tax rate seems almost impossibly high in the modern era even though it is only about half of what it was for nearly half of the 20th century. Proponents of supply-side economics claim success by arguing that incomes of wealthy people skyrocketed after taxes dropped on wealthy Americans. They tend to believe that people’s pay represents their productivity and so if rich people are getting paid more, then it must be due to higher productivity and higher productivity should benefit us all. The theory says rich people are the main job creators and if they get more productive, they will create more jobs to help all Americans.

Supply-side economics has been an unqualified success for the rich, but what about the rest of America? The fact is that median income has grown more slowly after taxes were lowered for the wealthy. The entire economy also grew more slowly and although that might be due to other factors, supply-sider cannot give evidence that lower taxes on the wealthy boosted their wealth enough to trickle down to help the middle class.

Economists like Greg Mankiw believe that each person’s income roughly represents how much they contribute to society. This is called the marginal-productivity theory of wages. This theory is sometimes useful as a first approximation, but it is clearly inaccurate. For example, CEOs can increase their incomes by making their companies more productive (which is very hard to do) or by squeezing more profits out of their companies for themselves. When income taxes are high, there is less point in playing political games to squeeze more profits away from shareholders and employees because the government would get much of it anyhow. It is impossible to know exactly how much of soaring CEO pay was a reward for higher CEO productivity and how much was a reward for CEO shenanigans with corporate governance, but there is zero evidence that corporations became more productive when their CEOs’ pay soared.

Most people don’t realize that CEO pay peaked in 2000 and then plummeted and has never completely recovered, but again there is no evidence that CEO productivity is lower now than in 2000.

Leave a Comment