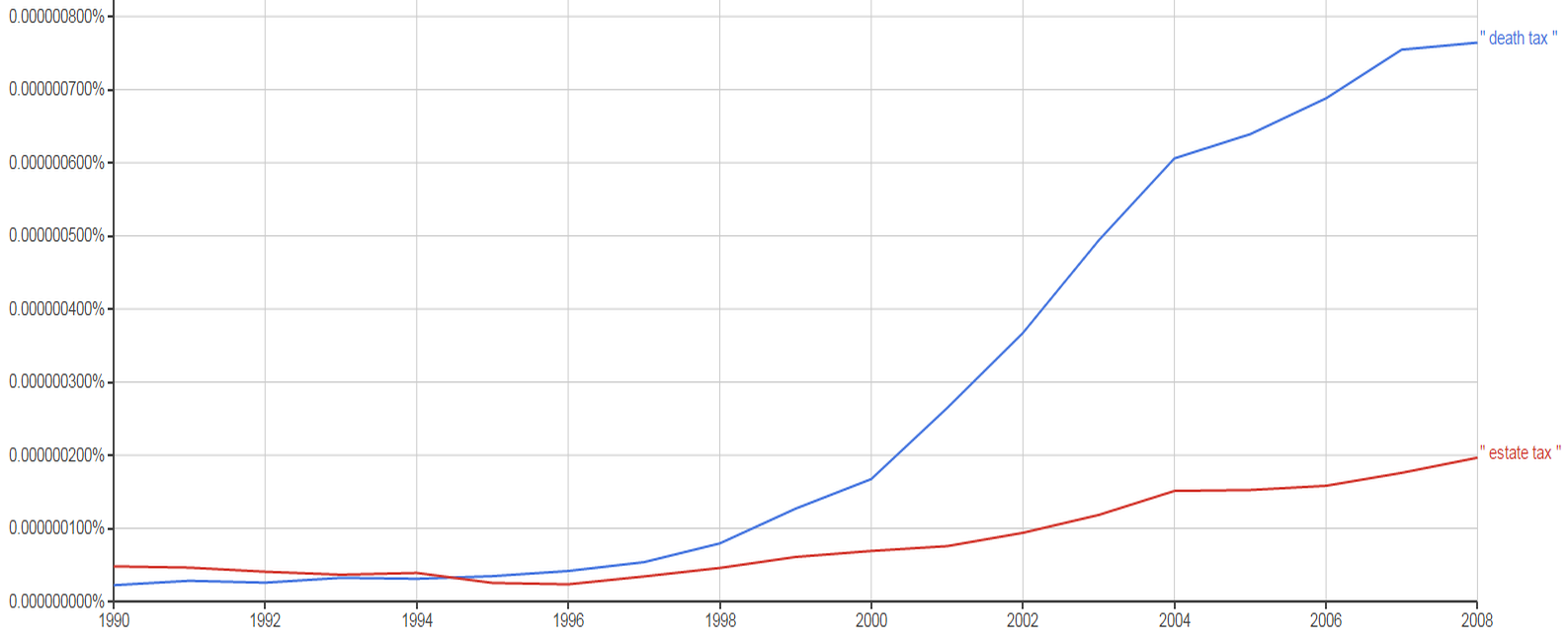

Most Americans think that the estate tax (popularly known as the ‘death tax’) should be reduced or eliminated. Wealthy families started funding a campaign in the mid 1990s which successfully rebranded this tax on large estates into a tax on death. Google’s Ngram Viewer shows how the term ‘death tax’ was half as common as the term ‘estate tax’ in written English in 1990. As of the most recent data the term ‘death tax’ has skyrocketed to become almost three times more common than the more accurate term.

It isn’t a “death tax” because, according to the Center on Budget and Policy Priorities (CBPP), “99.86 percent of estates owe no estate tax”, so perhaps a better name for it would be the dynastic estate tax since estates worth less than $24million for a married couple are not subject to the tax at all (as of 2022) and this is just the minimum exemption because there are many ways to hide even more money from the estate tax.

Republican pollster Frank Luntz promoted the term ‘death tax’ because it “kindled voter resentment in a way that ‘inheritance tax’ and ‘estate tax’ do not”. But ‘death tax’ is a misnomer because there is almost zero correlation between death and the tax. Only about 1 in 700 deaths are subjected to the estate tax.

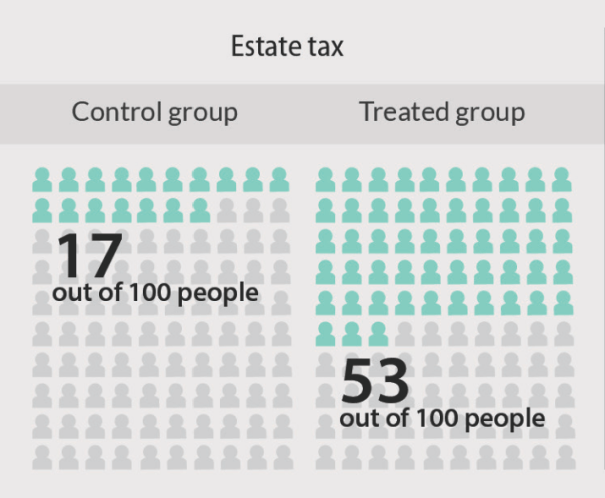

The Washington Center for Equitable Growth sponsored a poll showing that only 17% of Americans support the “Death Tax”, but when they learn that it only affects a little more than the top tenth of one percent of the wealthiest Americans’ estates, the majority (53%) supports it.

Jordan Weissmann says that the American public turned against the estate tax due to the success of the campaign to get Americans to think it is unfair to tax ordinary people when they die. Most Americans want to raise taxes on the wealthy, but they have been misled to think that the estate tax is a death tax that hurts most Americans at a time when they are already going through one of the most difficult times of their lives: death. The same campaign to rebrand it as a death tax has also spread the myth that it mainly hurts small businesses and farmers. When Americans learn that the estate tax really is a tax on extreme wealth, a majority supports it. Misinformation is the why American support for the estate tax has waned.

The Center For Effective Government (CEG) estimates that, “of the 2,662,000 Americans who died in 2013, just 3,700 of their estates paid any estate tax – one out of every 700 estates.” Of the estates that paid the tax, only 120 were family businesses or farms. Those were pretty rich farmers because in 2013 there was no tax on the first $5.4 million ($10.8 million for couples) of estate plus further exemptions that often save billions more through loopholes. In 2001 the American Farm Bureau Federation could not cite a single example of a farm having to be sold to pay estate taxes because most farms and small businesses have enough liquid investments on hand to pay the tax and the remainder can pay it gradually over 15 years. Dylan Mathews wrote about another study in 2005:

a 2005 analysis by the CBO found that under the 2009 estate tax, only 182 estates — and only 13 estates of farmers and 41 estates of people with family-owned businesses — wouldn’t have enough liquid assets (bonds, stock, cash, etc.) to pay their estate tax liability. The current estate tax law is even more generous than it was in 2009, meaning it’s likely even fewer estates are in that situation today. Moreover, as CBPP’s Huang and Brandon Debot note, “special estate tax provisions — such as the option to spread payments over a 15-year period and at low interest rates — allow the few taxable estates that would face any liquidity constraints to pay the tax without selling off any farm assets.”

The CEG estimates that if the government just collected the full value of the current estate tax on the 25 richest Americans, it would bring in $334 Billion in revenue. Just taxing the 25 biggest estates (if they didn’t evade the tax) would bring in enough to give a $10,000 inheritance (or tax cuts) to every child born in America for the next nine years! That could pay for a lot of college education. Here is the CEG’s list of how much the top 25 richest Americans would pay:

| Billionaire | Wealth Source | Wealth (in $ Billions) |

Estate Tax @ 40% (In $ Billions) |

| Bill Gates | Microsoft | 81.0 | 32.4 |

| Warren Buffett | Berkshire Hathaway | 67.0 | 26.8 |

| Larry Ellison | Oracle | 50.0 | 20.0 |

| Charles Koch | Inherited — Koch Industries | 42.0 | 16.8 |

| David Koch | Inherited — Koch Industries | 42.0 | 16.8 |

| Christy Walton | Inherited — Walmart | 38.0 | 15.2 |

| Jim Walton | Inherited — Walmart | 36.0 | 14.4 |

| Michael Bloomberg | Bloomberg plc | 35.0 | 14.0 |

| Alice Walton | Inherited — Walmart | 34.9 | 14.0 |

| S Robson Walton | Inherited — Walmart | 34.8 | 13.9 |

| Mark Zuckerberg | 34.0 | 13.6 | |

| Sheldon Adelson | Las Vegas Sands | 32.0 | 12.8 |

| Larry Page | 31.5 | 12.6 | |

| Sergey Brin | 31.0 | 12.4 | |

| Jeff Bezos | Amazon.com | 30.5 | 12.2 |

| Carl Icahn | Icahn Enterprises (private equity) | 26.0 | 10.4 |

| George Soros | Soros Asset Management | 24.0 | 9.6 |

| Steve Ballmer | Microsoft | 22.5 | 9.0 |

| Forrest Mars Jr | Inherited – Mars Candy | 22.0 | 8.8 |

| Jacqueline Mars | Inherited – Mars Candy | 22.0 | 8.8 |

| John Mars | Inherited – Mars Candy | 22.0 | 8.8 |

| Len Blavanik | Access Industries (private equity) | 21.5 | 8.6 |

| Phil Knight | NIKE | 19.9 | 8.0 |

| Michael Dell | Dell Computer | 17.7 | 7.1 |

| Laurene Powell Jobs | Inherited — Apple | 16.6 | 6.6 |

| Total | 333.6 |

But most of that wealth won’t be taxed for various reasons. For example, Bill Gates and Warren Buffett have exempted most of their wealth by directing their estates to give most of it away to charity.

Many of these people are in favor of the estate tax. For example, the CEG notes that ” Bill Gates, Warren Buffett, George Soros, and Carl Icahn have all campaigned publicly in favor of a high estate tax.”

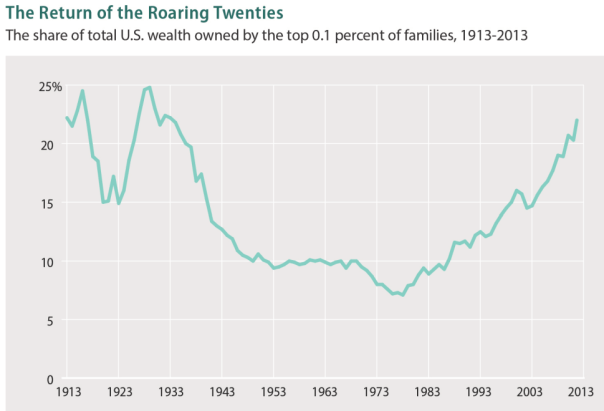

There is a well-documented cultural difference between rich people who were born rich and rich people who did not grow up in the top 1%. Billionaires who weren’t born rich and didn’t already feel the pinch of the inheritance tax are more likely to be in favor of the estate tax. In contrast all of the people on the list (underlined above) who inherited billions of dollars have given money to try to eliminate the estate tax. The one exception that proves the rule is Steve Job’s widow at the bottom of the list. But she was not born rich and did not pay any estate tax because spouses are exempt. Given that her philanthropic priorities include efforts to reduce inequality, she would probably support the estate tax because she is trying to give away most of her money and the estate tax is one of the best ways to reduce the inequality of the top tenth of one percent richest Americans as shown here:

Forbes magazine is run by an old money family and has been campaigning to eliminate the estate tax. Ryan Ellis is part of the campaign and he claims that it is futile to try to tax the wealthiest Americans because:

The uber-rich can afford these “teams of lawyers and accountants” to “develop and exploit loopholes” for their clients. First and second generation business owners and family farmers cannot. As a result, Paris Hilton will be ‘death tax’ess owners will either have to pay the death tax or funnel scarce capital into their own little army of tax nerds and lawyers.

This is part of the campaign to make it seem like a regressive tax on small businesses, but it is not. “Startup business owners” don’t have a problem because the tax only affects multi-million-dollar estates and anyone with a multi-million-dollar estate can afford lawyers and accountants to help them exploit loopholes. Furthermore, “startup business owners” rarely have estates worth more than $22 million (the 2022 exemption for couples) and the few multi-million-dollar children who inherit expensive startups without exploiting the loopholes can always raise funds for the tax by selling shares to outside investors or by getting a loan. These are the same old-fashioned funding mechanisms that most startups have to use. Approximately zero startups get their money from daddy’s death.

And if the problem is tax evasion, then the solution is simple. Eliminate loopholes so that Paris Hilton has to pay. As long as there are tax loopholes then it isn’t fair to the thousands of multimillionaires who dutifully pay the tax that some scheme up ways to evade it. Ellis says estate tax evasion is a problem, but he wants to abolish the tax which is tantamount to universal tax evasion.

Ellis also says we should eliminate the estate tax because it “collects almost no tax revenue” and is “a declining source of federal revenue”. True, the estate tax generated more than twice the revenues before his campaign succeeded in reducing it. The top estate tax rate fell from 77% in 1976 down to zero percent in 2010. It is back up to 40% now which is only about half its peak rate, but the effective rate is much lower today than it was during most of the golden age of America’s middle class wage growth. Ellis argues that the past success of his campaign to reduce the estate tax is a reason to reduce it further because they have already shrunken the tax down so small that they might as well kill it off.

Ellis dismisses the debate over the estate tax as “class warfare,” but all debates over tax policy are always class warfare. That is what makes tax reform so hard to do. Ellis demonstrates that “the uber-rich” have been winning the class war over the estate tax, and he concludes that ordinary Americans should surrender and let inheritance continue to increase inequality as it has since the 1970s. Sadly, most Americans agree with him because his campaign has succeeded in fooling most Americans into thinking that the estate tax increases inequality by hurting small businesses while the Paris Hiltons evade the tax.

Raising the estate tax would encourage more investment in meritocracy and less expenditures on lavish consumption for heirs. Currently, there is little point in investing in the human capital of heirs like Paris Hilton*. She doesn’t need an education because she will never need to work. Perhaps that is why she dropped out of high school. A bigger inheritance tax would help produce more imperative to invest in children to help them learn to earn future wealth and status rather than just giving them money. Because wealthy elites have disproportionate ability to set social norms, if the scions of the wealthiest elites spent more time working and less time partying, some of that ethos is likely to trickle down to the merely well-off.

*A backstory about inheritance within the Hilton family is that Paris’ great-grandfather, Conrad Hilton was the entrepreneur who made the family fortune, and he had planned to leave 97% of his estate to charity, but his son Barron contested the will and kept most of the fortune for himself instead. Thirty years later, Barron said he had become embarrassed by his granddaughter Paris’ behavior, and he would give 97% of his estate (estimated at $2.36 billion) to charity, which would leave his heirs with only 71 million dollars. But we will see if his heirs follow the family tradition of contesting the will when the time comes to keep the gravytrain flowing.

A higher estate tax would encourage more charitable donations and make it less lucrative for heirs to subvert the wills of the deceased.

[…] UPDATE: See “Death Tax” worse than an “Estate Tax” […]