Updated 2018/01/26

Unlike the natural sciences, macroeconomic ideas have implications that can dramatically redistribute wealth. That makes macroeconomics much more political than the natural sciences (with the exception of climate change) and the left–right political spectrum between progressives and conservatives has created divisions in macroeconomic theory. The media loves to present one dimensional yin-yang news stories with a simple two-sided narrative for every issue. That false dilemma narrative misrepresents the true nature of academic debates which often have tremendous consensus and multifaceted dimensions. This is true of policy-oriented macroeconomics which has evolved a tremendous consensus around a Keynesian-monetarist core, but there are multifaceted disagreements all around the periphery of that core. Simon Wren-Lewis said that, “macroeconomics is often taught as if [political and] ideological influence was non-existent, or at least not important to the development of the discipline. I think doing good social science involves recognising ideological influence, rather than pretending it does not exist.” This article is an attempt to explain some of the surprising political divisions that influence debates over macroeconomics.

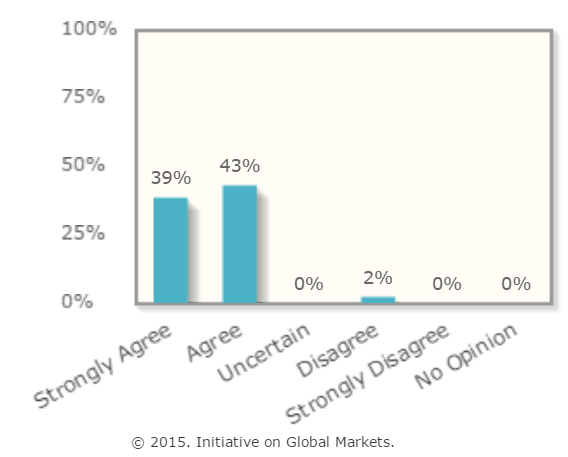

Overall economists are overwhelmingly Keynesian. Conservative economist Greg Mankiw’s pointed out in 2009 that 90% of economists agree that Keynesian fiscal policy works. Every poll of economists for decades has also shown tremendous consensus about this. For example, the University of Chicago polled elite economists in 2014 and found that 98% agreed that Obama’s fiscal stimulus worked to reduce unemployment:  All of the introductory textbooks teach the same Keynesian economics that yields this conclusion. The small minority of economists who reject the Keynesian model today are usually either completely focused on a discipline like finance that has nothing to do with macroeconomics and never teach it (like John Cochrane), or they are Real Business Cycle (RBC) theorists (like Robert Lucas). The RBC school does have an active research program at prestigious freshwater schools and has been very successful in publishing in top journals, but this school is insular and has rarely engaged with policy makers or with the vast majority of economists who reject RBC. RBC theorists can’t even teach introductory macroeconomics because none of them have figured out how to explain their theories in English without extremely complex mathematical models and dubious assumptions. As far as I know, almost all of the freshwater schools that are dominated by RBC theory in their graduate programs still teach Keynesian economics to their undergraduates because that is THE standard in undergraduate education.

All of the introductory textbooks teach the same Keynesian economics that yields this conclusion. The small minority of economists who reject the Keynesian model today are usually either completely focused on a discipline like finance that has nothing to do with macroeconomics and never teach it (like John Cochrane), or they are Real Business Cycle (RBC) theorists (like Robert Lucas). The RBC school does have an active research program at prestigious freshwater schools and has been very successful in publishing in top journals, but this school is insular and has rarely engaged with policy makers or with the vast majority of economists who reject RBC. RBC theorists can’t even teach introductory macroeconomics because none of them have figured out how to explain their theories in English without extremely complex mathematical models and dubious assumptions. As far as I know, almost all of the freshwater schools that are dominated by RBC theory in their graduate programs still teach Keynesian economics to their undergraduates because that is THE standard in undergraduate education.

Conservative Academic Macroeconomics

On the Right, the macroeconomists involved in government policy and business forecasting are almost all Keynesians,

The Keynesian School: Conservative Keynesians tend favor tax-cuts whereas liberal macroeconomists tend to be more amenable to increasing government spending and conservative spending priorities tend to be different from those of the Left. For example, conservative Keynesians are a bit more likely to promote military spending as a stimulus. This is sometimes called military Keynesianism, and it is also fairly popular on the Left.

Conservative Keynesians have dominated the list of economic policy advisors for every Republican president going back to at least the Ford administration and Republican candidate (post primary) that I can recall. For example, McCain’s chief economic adviser, (Doug Holtz-Eakin) and Romney’s (Glenn Hubbard) were Keynesians as were all of George W. Bush’s and George H.W. Bush’s advisors. Donald Trump has broken somewhat with tradition in that his long list of economic advisors was dominated by Wall Street investors rather than macroeconomists and his chief economic advisor, Kevin Hassett, has macroeconomics ideas that are as almost as hard to pin down as Trump’s. Hassett was for a Keynesian stimulus during George W. Bush’s administration, and then turned around and was one of the minority (demonstrated by the graph above) who argued against Obama’s Keynesian stimulus even though he simultaneously argued for the Obama administration to directly hire workers which is radically Keynesian. Hassett’s projections for the stimulative power of Trump’s corporate tax cut are now much greater than the consensus of mainstream economists. Although Kevin Hassett’s macroeconomics are hard to pin down, he is pretty consistently in favor of deficit-financed tax cuts. The American Conservative Magazine wrote that,

An astonishing number of the Republicans’ most cherished economic thinkers can be called Keynesians…. What is a conservative Keynesian? While there may not be a formal definition—mainstream Keynesianism has many nuanced variations—it is fair to say that a conservative Keynesian 1.) looks at the world in terms of macroeconomic aggregates, that is, total output, total employment, and most especially aggregate demand; 2.) sees government fiscal policy as a way to improve those aggregates; and 3.) embraces or at least tolerates deficit spending and inflation in the short run. That much is pretty close to standard Keynesianism. What makes one a Keynesian of the Right is a preference for tax cuts over government spending, although the intention is the same: to put money into the hands of consumers as a way to increase aggregate demand during recessions.

The Monetarist School: Monetarism was a relatively short-lived movement that peaked in the 1970s led by Milton Friedman. Many textbooks still present the 1970’s debate between monetarism and Keynesianism as being unresolved, but the academic debate ended in the 1980s and monetarism substantially ceased to exist as a separate school by the 1990s because Friedman’s band of monetarists won the key points of the debate and their ideas were adopted by Keynesians. The main legacy of the monetarist movement has been to prioritize monetary policy over fiscal policy for fighting recessions and became more focused on reducing inflation. Paul Krugman calculated that in the first 15 years after the debate ended, between 1985 and 2000 only five of the 7,000 or so papers published by the National Bureau of Economic Research mentioned fiscal policy in their title or abstract.

In some ways, the ideological split between Keynesianism and Monetarism was never very big. Keynes’ self-proclaimed followers had been ignoring some of his ideas about monetary policy that Friedman brought back to the fore. Some textbooks present monetarism as a free-market alternative to Keynesianism, but there really isn’t anything free market about it. This misconception probably stems from the fact that Milton Friedman happened to be a staunch free-market libertarian, whereas some of the prominent Keynesians that he debated (like Paul Samuelson who famously fought Friedman in Newsweek during the period) happened to be liberals. Part of Friedman’s motivation was to counter liberal Keynesian calls for government spending stimulus by promoting monetary stimulus instead. Some libertarians on the right continue to portray Keynesian economics as ‘central planning’ and call fiscal policy ‘socialism’, but they are a small minority and Friedman never thought of monetary policy as a realm that free markets should control. He recognized that monetarism is a form of central planning in which the government planners at the central bank adjust the quantity of money to control interest rates and inflation. (Inflation is the most fundamental price in the economy, the price of money.)

Monetarists wanted to fine-tune interest rates and inflation in order to stabilize the financial sector, unemployment, and economic growth. The Austrian libertarians reject monetarism and want to return to the gold standard because monetary policy is just as socialist as fiscal policy. Under the gold standard, central bankers have less control over monetary policy which is partly controlled by the gold market. Unfortunately for the libertarian purists, even on the gold standard, central bankers and financial regulators could still assert tremendous control over monetary policy because of the fractional reserve system that used paper money and bank accounts for most money. Gold was simply a symbolic base. Central banks (and other big institutions in the financial system) still actively manipulated the money supply under the gold standard and whenever the gold market made movements that they didn’t like, the central bankers just suspended it, so the gold market was never completely in control.

Today there are very few economists who still call themselves monetarists, and those who do tend to have a very strong preference for monetary policy over fiscal policy, but their theories for how monetary policy affects the economy is a standard part of modern Keynesianism. People who identify as monetarists have always tended to be more conservative than average, but there isn’t anything inherently conservative about monetary policy and libertarians have been trying to figure out how to avoid central banking for well over a century. This is part of the appeal of crypto-currencies like bitcoin to libertarians. Crypto-currencies don’t need to be controlled by any central authority unlike all other financial systems of equivalent sophistication.

The Real Business Cycle (RBC) School: Also known as the “new classical school”, freshwater economics, etc. This is the biggest academic challenge to Keynesianism and many top graduate schools like the University of Chicago and academic journals (like the journals the University of Chicago publishes) have completely abandoned study of Keynesian economics in favor of RBC macro, but the school didn’t do much study of recessions before the Great Recession of 2008 because RBC only became a major force during the Great Moderation of the mid-1980s until 2008 and there were no big recessions to investigate during this period.

RBC is a utopian form of macroeconomics that created extremely complex mathematical models of the economy that assume the economy is always in an equilibrium where everyone is making the best rational that they possibly can. Thus, RBC led to the “policy ineffectiveness proposition” which is the idea that monetary and fiscal policy cannot work to stabilize the economy. RBC models usually assume that monetary policy has zero effect on the real economy! This is an utter rejection of monetarism which is surprising because the University of Chicago was the ground zero of monetarism in the 1970s under the leadership of Milton Friedman. Friedman must be rolling in his grave with the knowledge that his former school has so utterly rejected his macroeconomics. RBC mainly gained ascendance for aesthetic reasons. It seemed to integrate microeconomics and macroeconomics. It uses complex, but elegant math. It was more consistent with the ethos in microeconomics at the time that assumed people are rational actors.

But it is also appealing for people who like the idea that markets naturally self-correct because it rejects the idea that a recession is a form of market failure. Some RBC models also gave some support to the idea of Ricardian equivalence which is the theory that fiscal policy has no effect on aggregate demand. Ricardian equivalence relies on false assumptions and is overwhelmingly contradicted by empirical research, but somehow it became fashionable in some RBC circles and once the Great Recession of 2008 happened, many prominent politicians and pundits (and very few economists) twisted it into a rationale for austerity and it morphed into a sort of “Austerian School” that became prominent in the popular press (see below).

Some RBC scholars are libertarians who believe that recessions are natural and inevitable and that government policy changes can only make them worse. Others are just ivory-tower geeks who love the math and don’t care about policy and politics

Austerian School (or liquidationists): These are terms of derision for Austrians and some RBC economists who think that the government should fight the recession through the opposite of Keynesian (and monetarist) policies. Austerity is reducing deficits and the money supply and austerians prescribe the exact opposite of the Keynesian recommendations.

There is nothing inherent about RBC models to support the idea that austerity can reduce recessions, but the RBC models are flexible and can yield wide-ranging results. The Austrian School (Hayek and Schumpeter) promoted austerity during the Great Depression, but they lost credibility because of it and Hayek completely abandoned his work on macroeconomics as a result.

Austerians often employ a traditionally Keynesian argument about confidence to give anti-Keynesian conclusions. They argue that recessions happen when people lose confidence due to worries about government inability to pay back government debts and worries about inflation. They think that if governments cut spending and reduce the money supply (to reduce inflation), people will regain confidence and start buying again and increase aggregate demand. Austerity has had wide populist appeal outside of the economics profession and although only a very small percentage of economists are Austerians, the ideology was popular among some of the leaders of elite institutions like the European Central Bank, the Bank of International Settlement, and the OECD during the early years of the Great Recession.

There is no formal economic model that supports the austerian view. It is not part of mainstream RBC academic theories. It was mainly an ad-hoc position that arose in response to the Great Recession of 2007. A couple of academic papers got a huge amount of press and political attention during the Great Recession for claiming to find empirical support for expansionary austerity, but they were all discredited when the authors allowed their data to be examined by peer review.

Centrist Independent Macroeconomics

Centrist academics are mostly Keynesians although there are also RBC scholars who just don’t care about politics and macroeconomic policy and just want to be left alone to do their work on their research that they love. The business economists who do macroeconomic forecasting for private industry are all Keynesians. RBC doesn’t even try to compete in the private sector.

Liberal Academic Macroeconomics

On the left, academic macroeconomics is a bit more dominated by Keynesians than on the right, but the left has different priorities.

Keynesian School: Liberal Keynesians are more favorably predisposed to government spending than conservative Keynesians who are more likely to favor tax cuts as an economic stimulus. There are a lot of sub-categories of Keynesians on the left, but their policies tend to be broadly similar:

Neo-Keynesian, Old-Keynesian, or Neoclassical Keynesian: This was mainstream macroeconomics from 1936-1980 that used simple the simple models that we still teach in undergraduate education based on things like AS-AD, Hicks’ IS-LM model, and the Phillips curve.

New-Keynesian: Use the complicated new mathematical modelling techniques developed by RBC, but add ‘frictions’ like sticky prices to get very similar results as the old Keynesians. They use completely different mathematical models and come to very similar conclusions.

Post-Keynesians: I don’t get why they think they are different, but they are more liberal than the mainstream and it seems to be a way for some liberal economists to signal their identify a bit like the monetarist label for some conservative economists.

Monetarist Keynesians: Liberal economists usually don’t call themselves monetarists, but Friedman won the intellectual debates over the role of monetary policy and almost all liberal economists embrace monetarist solutions as the primary tool for macroeconomic management. Keynes himself supported monetary stimulus, so It seems odd that there was ever an intellectual divide back in the 1970s between conservative-leaning monetarists and liberal-leaning Keynesians.

Agnostic-Apathetic ‘School’: There are a few economists on the left who simply have little opinion about macroeconomic debates because they did not study recessions in graduate school. They either chosen to ignore macro in favor of micro or they believed that recessions are not important in comparison with studying economic growth, international trade, or finance. I would put Jeffrey Sachs in this camp. He is a brilliant liberal development economist who wrote stupid things about the recession because he clearly did not put much thought into it. His priorities simply lie elsewhere. Unfortunately, Obama had economic advisers who are in this camp like Jack Lew and Tim Geithner, but they were not economists. They were Wall Street elites. They went along with calls for austerity because they thought it was politically popular and they did not prioritize fighting unemployment. The big ideological divide in the Obama administration was between the Keynesians at his Council of Economic Advisors and the Wall Street types who didn’t care much about macroeconomics who Obama put in charge of the Treasury.

Macroeconomics ideology at PhD-level education and research

PhD programs became divided in the 1970s, first between old Keynesians and monetarists and later between Keynesians and RBC. I have never fully understood the old Keynesian-monetarist debate because the two ‘schools’ are so integrated today that I have a hard time imagining why there was ever significant debate between the two. Keynes himself had monetarist ideas and the principle monetarist, Milton Friedman had written, “We are all Keynesians now.” Friedman wrote that in 1965, which was before the word monetarism had even been coined. He recognized that there was validity in Keynesianism, but macroeconomics is always imperfect and he did a lot to improve Keynesian thought.

Then in the 1980s, RBC began to displace Keynesian AND monetarism in freshwater PhD programs like the University of Chicago and the University of Wisconsin. These programs have a reputation for being conservative, but many liberals also graduated from these programs and followed the RBC research program which isn’t inherently political. Paul Krugman coined the term ‘freshwater economics’ to describe these inland schools where RBC displaced Keynesianism because the coastal schools, including most of the Ivy League, continued to teach Keynesian macro. These so-called saltwater schools were not much more liberal than the freshwater schools and they produced most of the conservative economists who went on to run economic policy for the Republican party (mentioned above).

Politicians ignored the freshwater (RBC) economists because they said that government policy is ineffective at best or counterproductive at worst. It was only natural for politicians to ignore the freshwater economists who said that there are no answers to our macroeconomic problems when there were many prestigious saltwater economists who claimed that they did have answers.

Whereas few undergraduate macroeconomics textbooks even try to explain RBC, there are two RBC graduate-school macro texts written by Ljungqvist, & Sargent and by Stokey, Lucas & Prescott. There are also some New Keynesian graduate texts that also teach RBC because RBC is generally just a simplified version of New Keynesian models.

The Austrian Business Cycle theory is “now rarely discussed by mainstream economists, but was actively debated” in academia before the Great Depression demolished the theory. Even its most revered scholar, Friedrich Hayek, gave up on working on it after the Depression. Austrian theory is still important in popular culture because of libertarian supporters who get a lot of media coverage. One libertarian group spent big bucks producing a pair of rap videos to try to boost its importance in grass-roots culture.

This theory is sometimes known as the hangover theory because recessions are caused by excessive and unsound investment during a boom. Recessions are necessary way to liquidate the excess capital stock and should be welcomed. This may have been where President Herbert Hoover and his Secretary of the Treasury, Andrew Mellon got their theory that it was productive to “Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate .… It will purge the rottenness out of the system. High costs of living and high living will come down. People will work harder, live a more moral life.”

One of the major problems with the Austrian theory is that it predicts that, “people will work harder” during a recession. It fails to explain unemployment. If a recession were caused by an excess of capital, then demand for workers should increase during a recession rather than decrease, at least in large sectors of the economy.

The Austrian theory was an advance over the classical view of economics in which recessions were impossible, but it agreed with the classical view that there is no point trying to use fiscal and monetary policy to fight recessions because in the Austrian view, a recession is a good thing that must continue until the excess capital and unproductive businesses are destroyed so that, in Hoover’s words, “enterprising people [can] pick up the wrecks from less competent people.”

There are still libertarians who ascribe to this philosophy. For example, President Trump’s chief economic adviser Larry Kudlow welcomed the Great Recession, writing as the economy was beginning to crash in 2008: “Recessions are therapeutic. They cleanse excess from the economy. Think about excessive risk speculation, leverage, and housing. Recessions are curative: They restore balance and create the foundation for the next recovery.”

At the PhD level, the last university in the world that focused on Austrian theories was Auburn University, but it’s PhD program was disbanded in 1999 and they apparently did not put much stock in Austrian macroeconomics because they didn’t have anyone who taught macroeconomics! The Austrians agree with many of the conclusions of the RBC theorists. Both schools think that recessions are naturally the best of all possible worlds and nothing can or should be done to try to lessen them. But the Austrians reject RBC theory because they dislike the mathematical methods of RBC. Austrians tend to favor the gold standard which is something that the RBC economists reject.

Macroeconomic ideology in undergraduate education

Almost all of the undergraduate textbooks present the standard Keynesian-monetarist synthesis whether they are written by a conservative Republican like Ben Bernanke or a liberal Democrat like Robert Frank. Oh wait. Those guys co-authored the same textbook which presents roughly the same Keynesian-monetarist synthesis as the top-selling text by conservative former adviser to Bush and Romney, Greg Mankiw (who named his dog Keynes) and the text by liberal lightening-rod Paul Krugman. The only alternative to the textbook consensus comes from Real Business Cycle (RBC) theory, but it only appears in very few textbooks that haven’t sold well. As mentioned above, RBC has been very successful among some top economics researchers in PhD programs, but it never made much headway in the undergraduate education even at the RBC schools because it is too mathematical for undergraduates to comprehend. It takes a PhD to think you understand RBC, but even the PhDs have not really understood how to apply their own models. The math was just so complex that they did not completely understand their own theories and the entire RBC agenda fell apart during the 2008 recession.

My first Macroeconomics prof in grad school, Paul Peiper, was a Keynesian who often said that you should be able to explain your mathematical model in plain English to a smart undergraduate and if you can’t then you probably don’t understand your own model well enough. I suspect he was thinking about RBC theorists who simply cannot explain their models to undergraduates.

The old Keynesian stories about the economy always made empirical sense and can be explained to undergraduates, so RBC was never able to displace Keynesianism in undergraduate education. New Keynesian models are built on the same kind of math as RBC, but they produce the same results as the old Keynesian stories so there was no need to change the textbooks.

A conservative website I read asked for examples of conservative economics texts, and readers submitted suggestions for about 30 popular books, and two graduate-level RBC texts (mentioned above), but not a single undergraduate macroeconomics textbook. Both conservative and liberal economists mostly teach Keynesian macroeconomics to undergraduates.

Some undergraduate textbooks mention “supply-side economics,” but that isn’t an academic school at all. It is a political movement that gained momentum in the 1970s based on Arthur Laffer’s resurrection of the idea that cutting taxes would create so much growth in aggregate supply that it would pay for itself and increase revenues. If you search the primary academic journal archive at Jstor, you will not find any references to a “supply-side school” or even “supply-side economists” except in commenting on the popular political movement.

This supply-side idea was also once promoted by Keynesians who influenced JFK’s tax cuts in the 1960s (from a top income tax rate of 91% down to 70%) and Keynesians still have a similar theory that a tax cut during a recession can restore economic growth enough to more than pay for itself if the multiplier is big enough. Conservative Keynesians often make this argument and it was the basis for George Bush’s tax rebate checks in 2008. The difference between the Keynesian theory and the supply-side theory is that in the Keynesian theory, tax cuts stimulate aggregate demand during recessions by reducing hoarded savings whereas the supply-siders think tax cuts always cause an increase in aggregate supply (productivity) by making people work a lot more hours and create more capital. Also Keynesian economists predict that tax cuts would only boost the economy during a recession and supply-side activists always predict that it would be good for the economy, even during an economic boom. Very, very few academic economists subscribe to this core supply-side idea.

Macroeconomic media bias: “Mediamacro”

Most of the general public develops an understanding of science from the popularizers of science like Steven Hawking and Neil deGrasse Tyson because very few people get a science degree. But at least most people formally study basic science in high school and college graduates get at least a couple classes. Only a tiny minority has ever had even a single macroeconomics course at any level and most people develop their understanding of economics from popularizers in the mass media who are disproportionately hacks.

Whereas interest groups ignore most scientific disciplines with a few exceptions like global warming and medicine, moneyed interests have taken a great interest in economics and injected hacks into popular discussions.

Simon Wren-Lewis calls the mainstream media’s view of macro, “mediamacro.” The media had particular biases during the 2008 crisis. For example, the media was much more austerian than either the general public or the economics profession. The media loves to oversimplify and use inappropriate moral analogies like to say that the government needs to be less lazy and borrow less money so that we don’t put a debt burden on our children. Big media is also biased towards the opinions of powerful business people who buy advertisements, and own media companies. The media is also overly enamored with the opinions of Wall-Street tycoons who have never studied macroeconomics.

Controversial ideas sell more advertisements than consensus, so the media likes to promote provocative macroeconomic hacks rather than the the boring consensus that readers could get in any textbook or even on Wikipedia. The media likes crazy ideas because crazy people are interesting and the media likes to tell simple narratives about 2-sided debates. If the media cannot find enough debate among PhD economists, they will try to find someone else, even if they have to find a madman. Crazy people certainly say interesting things that can be fun to watch. Anyone can call himself an economist and most of the ‘economists’ on the TV news are not qualified to teach undergraduate economics because they do not have any economics degree. And when the media does interview someone with an actual economics degree, there is a bias towards interviewing economists who work for an interest group whose job is to seek media influence unlike academics.

That is how the gold standard gets so much attention in the media despite almost zero support from economists. Less than 1% of PhD economists think that the gold standard is better than our current system (and most of them probably went to Auburn University, mentioned above), but the press loves the gold standard because it is interesting and simple. The media loves opposing viewpoints so they can claim “balance” so they present madmen arguing for the gold standard to “balance” against some boring guy representing the entire economics profession who thinks it is a terrible system. Media bias helps explain why 44% of Americans think a return to the gold standard would be a good idea.

The media likes to tell stories about conflict between two sides of any issue. More than two sides gets too complicated for the narratives that they try to create, so they tend to engineer simplistic narratives that are more entertaining than the difficult complexities of reality. In the most simplified (and unrealistic) media narrative, the liberals are Keynesians who support government spending and the conservatives are anti-Keynesians who support business interests by shrinking the deficit. This is a misleading narrative that contains only the tiniest grain of reality. Macroeconomics is political, but the true ideologies of the various factions are more complex.

Two main reasons for the political divisions in macroeconomics:

1. Macroeconomic policies divide classes and create winners and losers.

Monetarist policies would raise inflation and lower real interest rates during recessions which hurts savers (richer and older) and benefits borrowers (poorer and younger). Keynesian deficit policies tend to worry the wealthy more than the middle class because the wealthy are hurt less by high unemployment and they pay a disproportionate amount of the taxes that will eventually repay the deficits. Plus, Keynesian expansionary policies require redistributing resources from the class of people who are prone to hoard (richer and older) to people who want to spend (poorer and younger).

2. People have different ideologies about how the world works.

Keynesian-monetarist ideas assume that mass unemployment is due to a massive market failure. A minority of economists dislike the very idea of market failure because it is messy and unaesthetic. A few have an almost religious faith in the benevolence of markets. Economic elites also tend to dislike the idea of market failure because if markets can fail, then some of their wealth may be due to market failure. Business elites tend to like the ideology that perfect markets have rewarded them efficiently. It is a justification for their wealth and power over others. Under perfect markets, wealth would be a perfect reward for contributions to society.

Macroeconomic Political Divide Summary

There is no simple way explain the ideological macroeconomic divisions between Republicans and Democrats. The top-level economic advisers in both parties have been almost exclusively Keynesians all the way back to WWII. But politicians just do not listen to their economic advisers when it comes to making economic policy. Austerians have had tremendous anti-Keynesian influence over both parties despite not holding official positions of authority. Ever since 2008 when the economic stimulus package was passed, both parties have been austerian. For example, Obama raised taxes as part of the Affordable Care Act (Obamacare) so it would reduce the deficit and has been trying to raise taxes on the wealthy. That is austerian, not Keynesian. Similarly, the Republicans have been trying to cut social spending, and the Democrats seem to have been happy to let government spending decrease (as a fraction of our total income) since the beginning of 2009.

On the monetary policy side, Obama neglected to appoint Fed board members for months because he was shockingly apathetic about monetary policy. The Republican leadership criticized the Fed for trying to help reduce unemployment by expanding the money supply which was a rejection of Milton Friedman’s conservative monetarist ideas. Both parties displayed austerian monetary policy priorities.

Today there is no significant academic division between monetarists and Keynesians. The big ideological divide in academic macroeconomics is between both of them and the RBC economists who make radically different predictions. The RBC school thinks that the government cannot (or should not) do anything to help recover from recessions and RBC doesn’t suggest that there is any problem with austerity so some RBC scholars like the idea of austerity for various other reasons. What little monetarist-Keynesian ideological divide still exists is mostly one of priority. Economists who call themselves Keynesians generally put more priority on fiscal stimulus and think that works better than monetary stimulus, particularly when interest rates are near zero. The few economists who still call themselves monetarists put more priority on monetary stimulus and think that quantitative easing works better than fiscal stimulus. But most mainstream Keynesians endorse what used to be called monetarist ideas back in the 1970s.

There are a lot of self-taught Austerians who oppose the Keynesian-monetarist synthesis, but they are rarely qualified to teach undergraduate economics classes. In academic macroeconomics, only the RBC school has been a significant challenge to Keynesianism. Although the RBC vision has enchanted many bright academics, they had kept themselves withdrawn from policy discussions in their ivory-towers since according to RBC theory, policy either has no effect or certainly doesn’t help. They remained isolated from the challenging ideas of the world outside during the Great Moderation until the crisis of 2008 finally brought them challenges that they could not ignore.

Because Keynesian-monetarist policies are likely to improve the plight of the median American, I support this academic consensus. Keynesian policies should benefit both the needy (unemployed) and the median. Massive unemployment and idle capital is a tragic waste and we should use all effective tools to reduce the suffering. This should not be controversial. It is the textbook consensus that almost every college student learns in Principles of Macroeconomics. It is amazing to me how the media and both parties conspired to produce austerianism which is the polar opposite of the macroeconomics taught in the college textbooks.

{kind=link}