Updated 4/12/2018

Arindrajit Dube wrote a paper in 2004 that explains several ways that the minimum wage is flawed in the US, including:

- The minimum wage is too low.

- It isn’t adjusted for inflation.

- It isn’t adjusted for local cost of living and labor market conditions. In some places with high wages and costs (like Aspen, Colorado) it is laughably low.

Dube has a better way. He proposes to set the local minimum wage at half the local median wage. That would automatically adjust the minimum wage to the local labor market and help keep it adjusted for inflation. It would also raise the real value of the minimum wage up to the level where it was in the US in the 1960s and 70s and closer to the international average ratio of minimum-to-median in other OECD nations.

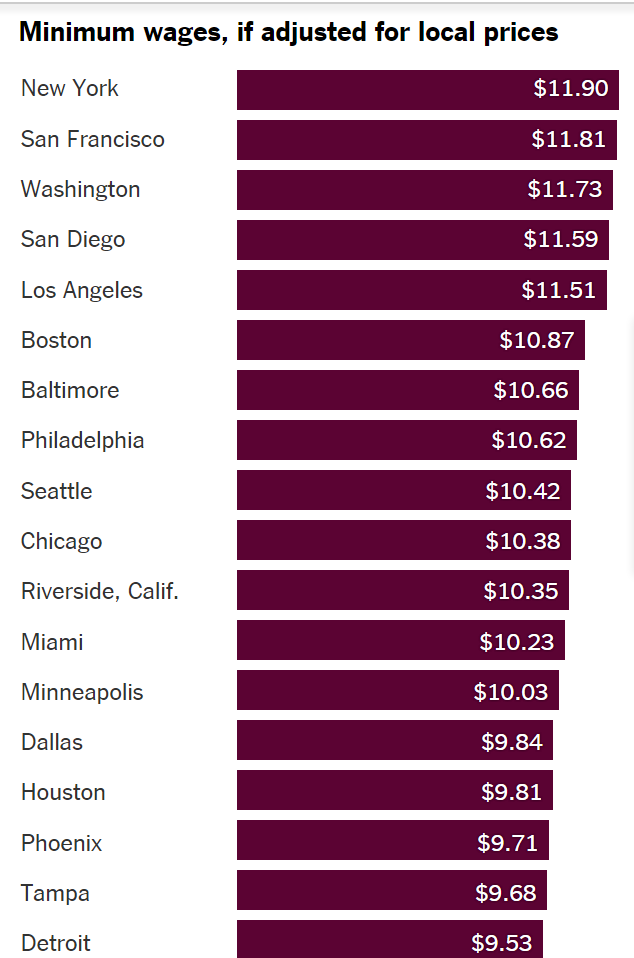

Jared Bernstein created a graph showing the effect of a proposal like this in a few regions of the US:

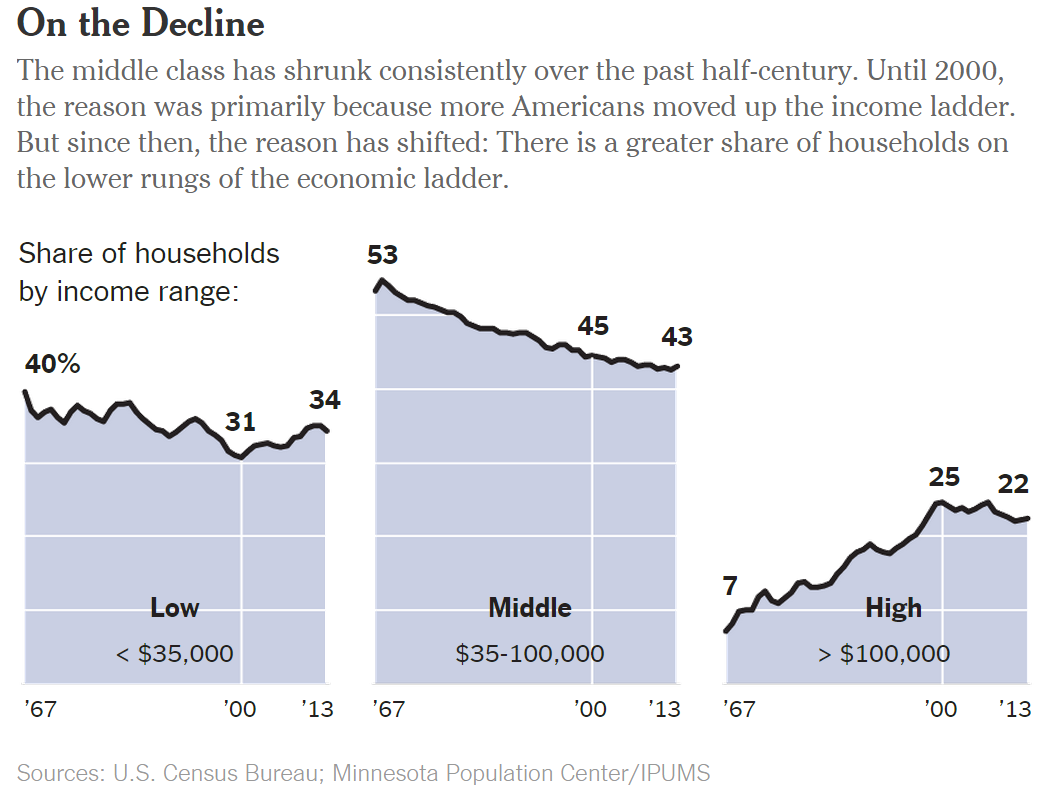

Many cities and states independently raise their local minimum wages to closer to half of the median wage because the federal minimum wage is just ridiculously low in high-wage places like New York City and San Francisco. Dube’s proposal would standardize this tendency across the US. Plus, businesses would be able to prepare for minimum wage hikes better if the process were standardized across the US and more predictable. When legislatures arbitrarily adjust the minimum wage for inflation they cause relatively large, abrupt changes that are harder for businesses to adjust to. In 1949, the minimum wage almost doubled and even small jumps can be hard to accommodate. When Ohio suddenly raised the state minimum wage in 2008, it pushed the budget into the red at Bluffton University’s (where I work) because it was a large, budgeted expense. Eliminating all the jagged increases on the graph below would create a more efficient system.

Opponents of the minimum wage might think that a less efficient system is better because an inefficient minimum wage system might be less politically popular, but they should face up to the reality that polls consistently demonstrate that the minimum wage is extremely popular among ordinary people in both parties, so neither party will commit political suicide and abolish it despite the constant lobbying of the Employment Policies Institute and the National Restaurant Association which contacted me in a covert effort to try to fight the minimum wage. Below is polling data showing the percent of Americans who favored raising the minimum wage and even extreme increases in the minimum wage poll favorably. A 2016 poll found that a majority of Americans favored more than doubling the minimum wage.

| Favor | Oppose | ||

| 2014 | 73% | 20% | |

| 2013 | Nov | 76% | 22% |

| 2013 | Mar | 71% | 27% |

| 2005 | 83% | 14% | |

| 2000 | 82% | 16% | |

| 1999 | 81% | 18% | |

| 1996 | 83% | 15% | |

| 1995 | 73% | 21% |

The Republican Party leadership has tended to oppose minimum wage increases over the decades, but ironically the Republican Party would have the most to gain politically from a proposal like Dube’s because it would eliminate the constant opportunities for their opponents to successfully bash them. Under the current system, as inflation erodes the real value of the minimum wage, it constantly builds more popular pressure to raise the minimum wage to adjust for inflation which eventually forces congress to pass legislation to increase it. The Democratic Party regularly gets a political boost when the minimum wage is in the news and the Republicans are stuck defending a very unpopular position. Dube’s proposal would eliminate the need to regularly pass laws to adjust the minimum wage for inflation and that would help the Republican leadership avoid an uncomfortable topic that regularly gives a boost to their opponents and that they always eventually lose anyhow. The minimum wage almost never comes up as a political football in countries where the minimum wage is indexed to inflation and conservatives can focus on other political issues that are more winnable.

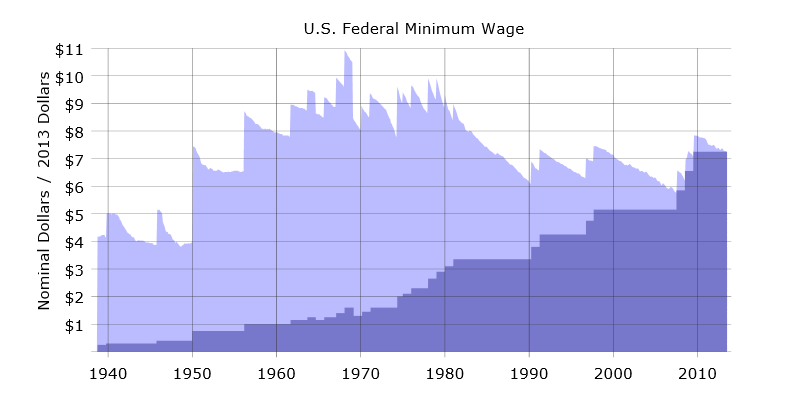

The CEPR wrote a history of minimum wage research which may help explain why the real value of the minimum wage dropped during the 1980s and stayed low since then (see the decline in the above graph in light purple). In the early 1980s a lot of the first empirical research was published about the effects of the minimum wage and most found that the minimum wage increased unemployment. However, the early research was done poorly and subsequent research using larger samples and more sophisticated techniques reversed the conclusions of the early findings. But the early research probably influenced policies at the time and helped those who argued for reducing the minimum wage. That is the power of ideas.

Economists were quite divided about whether the minimum wage was a good idea 20 years ago, because economists used to think that it hurt the poor by raising unemployment. But the empirical studies since the 1990s have overwhelmingly shown insignificant effect on unemployment, and by 2014, a University of Chicago poll found that elite economists were fairly evenly split on whether the minimum wage causes any unemployment at all and five times more economists supported raising it than opposed it. Below is graph from a meta-analysis of 1,492 studies about the effects of the minimum wage on unemployment that explains the mainstream view. Note the large spike at 0 meaning zero effect, plus a large number of studies to the right of zero that actually show that the minimum wage decreases unemployment slightly! Out of the 1,492 studies, only about 1% that have a large negative effect on unemployment. Those are the outliers on the left, but all of them have relatively low power and all of the most powerful studies show very close to zero effect on unemployment.

Doucouliagos and Stanley (2009) conclude that there is only an extremely small effect of the minimum wage on unemployment, saying, “If correct the minimum wage could be doubled and cause only a 1 per cent decrease in teenage employment.” That claim gives a vivid illustration of how trivial the effects of past increases in the minimum wage have been, but it is undoubtedly wrong about extrapolating from the past research to the potential effect of doubling the minimum wage. A doubling would be much larger than almost any past increase that has been studied. We only know that past increases have had little effect, but we do not know what would happen if we made a very large increase in the minimum wage. If we were to actually double the minimum wage, there could be a much bigger negative effect upon unemployment. The historical evidence just can’t tell us much about that because it would be so much bigger than what we have studied.

Dube’s proposal to set the minimum wage at half the local median wage is similar to what international businesses do. They adjust the wages they pay across the regions of the globe to reflect the going wage in different locations. For example, Ikea pays lower wages in areas that have lower wages and costs of living. The minimum wage should adjust to local labor market conditions as well. Dube’s proposal is also similar to the government’s method for setting the maximum CEO wage it pays to defense contractors and private prison corporations. Kevin Drum explains:

Apparently the federal government has a cap on the amount it’s willing to reimburse contractors for the salaries of their employees. If… your company’s CEO makes $3 million per year, you can’t charge it all back to the feds even if 100 percent of the CEO’s time is spent on government contracts. The limit, set in 1998, was $340,000.

[If that amount had risen with inflation], by 2011 it would be around $467,000. But no. It [rose to] $763,000. Why? Because ordinary inflation adjustments are for chumps, that’s why. For purposes of charging CEO overhead to the federal government, the cap was set at “the median amount of the compensation provided for the five most highly compensated employees of all publicly owned U.S. corporations with annual sales in excess of $50 million for the most recent fiscal year.”

This rule means that taxpayers have increased what we pay to the CEOs of government contractors much faster than inflation. The median wage and even the President of the US’s wage has not risen nearly as fast. CEO pay on the government payroll is rising fast because, as Lydia DePillis notes, the median salary of CEOs at America’s 3,000 largest companies has risen precipitously. By now, CEOs are billing taxpayers about double the salary of the highest paid federal government worker (the president at $400,000). DePillis argues that the government should worry more about raising the wages of the poorest people working for its contractors rather than the richest. She criticizes the Obama administration for not doing anything about the way its privatized corporate welfare for CEOs results in lower pay for ordinary workers and higher pay for elites:

Right now, the federal government employs some 2 million people [working for private companies paid by government contracts] who make less than $24,000 per year, or under $12 an hour. The administration could, by executive order, require that all of them be paid at least that.

Instead, Obama raised the rate to $10.10 in January 2015. Again, Dube’s proposal is more sensible. Just set the minimum wage for federal contractors at half the local median wage. Since it works for CEOs at the top, why use it for workers at the bottom too?

So who gets the benefits of a minimum wage hike like the one Obama made for federal contractors? A 2010 study by conservative economists estimated that only 11% of the benefits go to poor households and they argue that the minimum wage is a bad anti-poverty program that should be scrapped, but most of the benefits of the minimum wage go to middle-class households which is probably one reason it is so popular. An Economic Policy Institute study estimated that if the minimum wage were raised to $10.10 an hour, 77% of the benefits would go to households earning more than $20,000 per year and less than 69% would go to households below the median income. So the minimum wage does fight poverty a little, but it is more beneficial for the middle class than for the poor.

One reason why such high-income households see benefits from the minimum wags is that young people often get minimum wage jobs and many young workers live in middle-class households. The Bureau of Labor Statistics estimates that about 1/3 of minimum-wage workers are teenagers and Heritage estimates that 62% of young adults and teens earning the minimum wage are enrolled in school. Raising the minimum wage would help make college more affordable for them. Whereas the real value of the minimum wage was much higher in the 1960s and 70s, the cost of college tuition has risen faster than average. Until the 1980s, college students could earn enough to pay for tuition solely by working a minimum wage job during the summers. The horizontal orange line is at about 480 hours which is what a student would work in a three-month summer job at 40 hours per week.

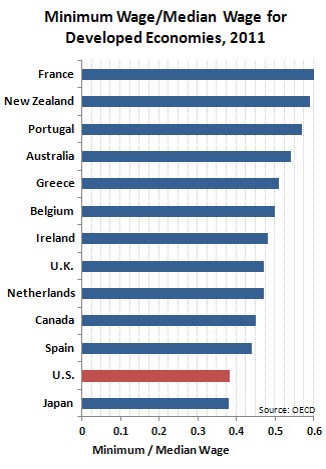

And raising the minimum wage up to half the median wage would put it closer to the level seen in many other rich nations:

Does the minimum wage increase inflation? Will it increase the cost of fast food? Jordan Weissmann says that it will, but not by much:

Sara Lemos reviewed the literature and found that most studies reviewed above found that a 10 percent US minimum wage increase raises food prices by no more than 4 percent and overall prices by no more than 0.4 percent.”

But what about burgers specifically? Well, their prices would might go up a bit more. Based on data from 80s and early 90s, Daniel Aaronson estimated that a 10 percent increase in the minimum wage drove up the price of McDonald’s burgers, KFC chicken, and Pizza Hut’s pizza-like product by as much as 10 percent.

This is wrong. A 10% increase in the minimum wage cannot conceivably increase fast food prices by 10%. You know the above quote is wrong because of simple back-of-the-envelope math, and if you look at the original research cited at the above link, you will see that it too claims that the minimum wage is associated with trivial increases in prices. The math just does not work for a 10% increase in minimum wage to increase prices by 10% because that would imply that minimum-wage labor is the only cost involved in producing fast food! For example, suppose it takes one hour to make one burger and McDonalds is selling burgers at cost. If wages are $10, then a burger will cost $10 if wages are the only cost of producing burgers. If wages rise 10%, then prices of burgers must rise 10%. But that is ridiculous because minimum wage labor is only a small fraction of the cost of producing burgers. The owners of fast food restaurants get paid considerable money to compensate them for the fixed costs of the buildings, advertising, equipment, etc. There are managers and accountants who get paid more than the minimum wage, and there is the cost of the meat, bread, packaging, cheese and other inputs that is produced in industries where minimum-wage labor is a tiny fraction of the total costs. Steven Buckley estimated that TOTAL labor costs in the restaurant industry vary from only about 25% of total costs in fast food up to a high of about 40% in table-service restaurants, and even that greatly overstates the effect of minimum wage labor because of the jobs that pay more than the minimum wage like supervisors, accountants, marketers, and others.

In the US economy as a whole, labor compensation is about 60% of total income, but less than 3% of HOURLY workers earned the minimum wage and high-income workers are not among the hourly workers. Because minimum wage workers earn a fraction of what the average worker earns, the share of total GDP that is accounted for by the minimum wage is undoubtedly far less than 1% of national income. Even if the minimum wage were increased 10% , it is unlikely to increase prices by a tenth of one percent which is unmeasurable relative to the inherent noise and uncertainty in our inflation measurements.

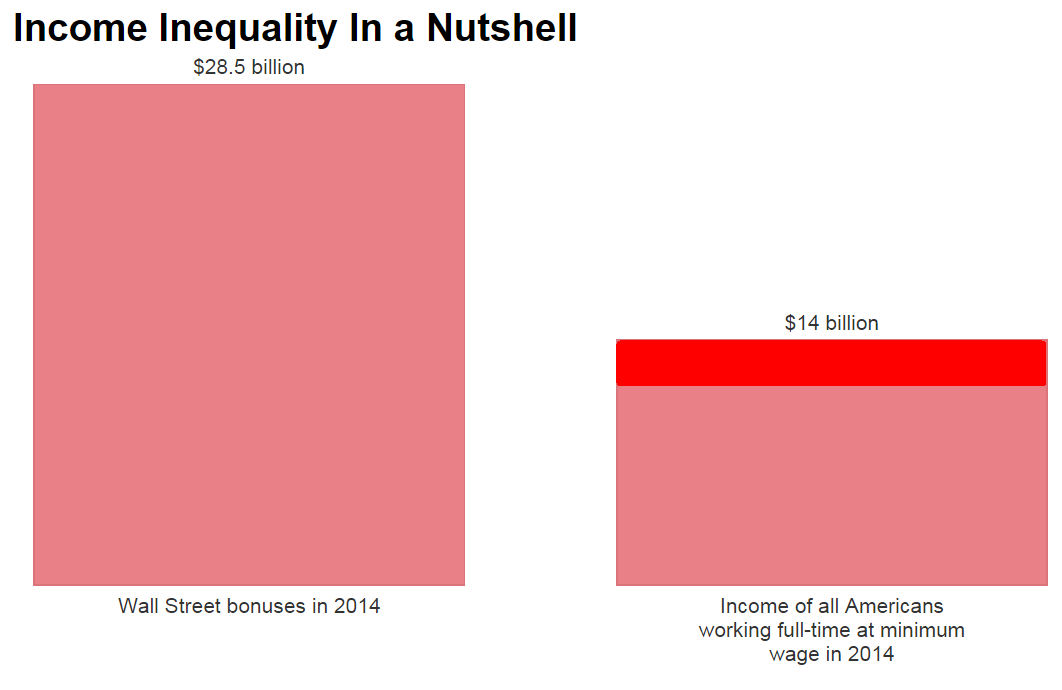

If you are worried about the effect of labor income upon inflation, you should be more worried about pay for elites because the minimum wage is simply a nothingburger in the US economy compared to the BONUSES of Wall Street. Here is data from The Institute for Policy Studies.

The left side isn’t measuring total Wall Street compensation. It is only executive bonuses on top of ordinary pay. And you shouldn’t compare that with the total income of full-time minimum wage workers because even without the minimum wage they would be paid most of that money anyhow because the minimum wage is pretty close to the equilibrium market wage. The minimum wage only adds a bit to the top of the wages that low-wage workers would have earned without a minimum wage. I added a little red rectangle that shows my guess at how much money the minimum wage might add to low-wage incomes. Bonuses were $28.5 billion versus maybe something like $3 billion that the minimum wage actually cost. The anti-minimum-wage lobbyists claim that they are worried about the detrimental effect of the minimum wage upon inflation and prices, but they should probably be more worried about Wall Street executive pay than about the pittance that low-income Americans earn.

Rice is commonly grown in small nursery plots in 5% of the field for a month or two before transplanting out into the rest of the field for the final months of growth. By transplanting the rice seedlings, farmers can grow three full crops per year in tropical regions. Transplanting rice isn’t an obvious technology to copy and intensive rice production requires many more techniques that are difficult to copy (like using

Rice is commonly grown in small nursery plots in 5% of the field for a month or two before transplanting out into the rest of the field for the final months of growth. By transplanting the rice seedlings, farmers can grow three full crops per year in tropical regions. Transplanting rice isn’t an obvious technology to copy and intensive rice production requires many more techniques that are difficult to copy (like using

FRED

FRED

{kind=link}

{kind=link}

{kind=link}