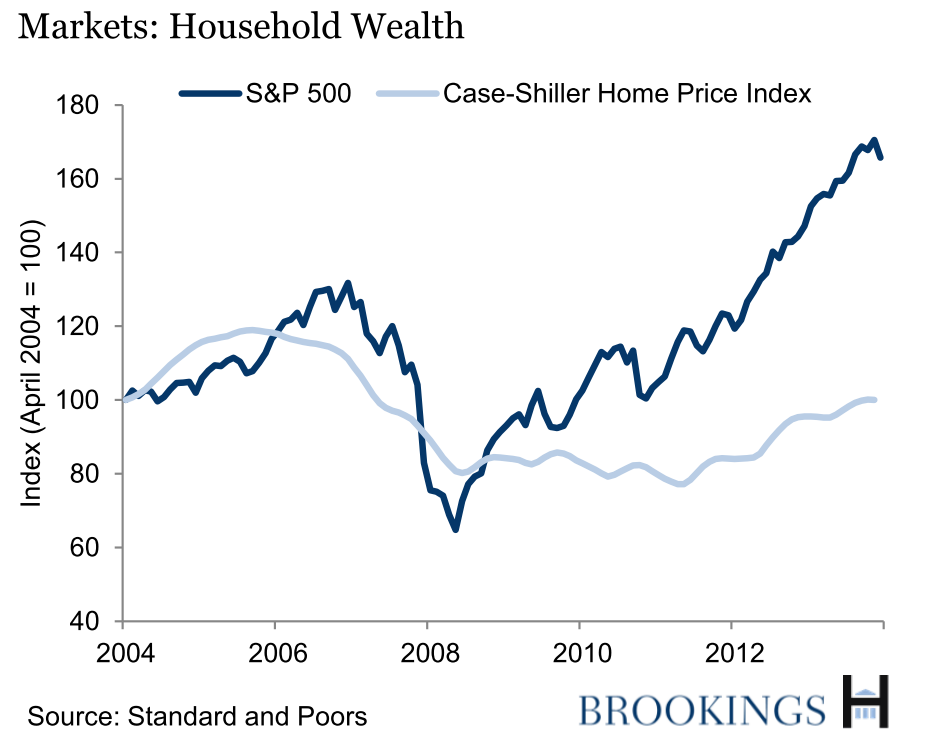

The Brookings Institution updated a good article earlier this month showing the dashboard that the Federal Reserve leadership uses to steer the US economy using the “most important[¡¿]” measures. This “array of gauges” gives useful information, but it lacks anything about the median American and some, like GDP, are particularly skewed towards the well being of elites. Even worse than GDP is what Brookings calls its measures of “household wealth”:

These measures are very far from measuring the household wealth of the average American. The median American has more wealth tied up in the rapidly depreciating vehicles in her driveway than in the stock market, so the S&P500 stock market index has little relevance to the median American.

The other indicator on the graph measures housing prices. That is much more important to median well being than the S&P500, but it is still a bad measure. This measure is inflated by including the total value of mansions and second homes in the total stock of housing wealth. Bill Gates’ homes are worth more than the equity of probably a third of American households, because almost a third of households rent, so a rise in the price of housing is purely bad for them. But even for most people who have bought a home, higher home prices do not help because most people only have one home and they need to live in it. A rising house price would only be useful for a homeowner who could find somewhere cheaper to live, but if all home values rise, then nobody can sell his home and become better off by finding a better deal somewhere else. Only people who want to downsize into a smaller home could benefit. At the extreme, someone who wanted to sell his house and became homeless would clearly benefit from higher housing prices, but this is a bit absurd. For most people, housing is a strongly normal good. That means that as wealth increases, they spend more on housing. Thus, as housing wealth increases, most people just spend more of their new wealth on the housing that they are already living in rather than downsizing, and they are no better off.

Housing is more of a consumption good than a store of wealth for most households. Only elites who have extra homes could see housing as primarily a store of wealth. The Fed leadership probably has extra homes because they are all well above the median income and they probably have fat stock portfolios too. When the Fed leadership uses housing and stock prices to measure economic wellbeing, they are using meaningful measures for elites like themselves, but not for the median. The Fed leadership doesn’t care about measuring their effect on the median American. And that is one reason why the Fed leadership doesn’t really care about unemployment either.