Secular stagnation usually refers to some sort of structural problem with aggregate demand that will maintain high unemployment along with low inflation and interest rates as you can see in this free ebook about secular stagnation written by famous economists. As Yglesias at VOX points out:

The most prominent alternative to secular stagnation is probably the technological slowdown hypothesis. This view, best represented in academia by Northwestern University economist Robert Gordon, in the business world by investor Peter Thiel, and in the popular press by Tyler Cowen, posits that slow growth is a structural phenomenon due primarily to a slowdown in the rate of technological progress. Cowen’s book the Great Stagnation is a good treatment of these ideas…

These ideas distinguish themselves from secular stagnation in that they are primarily ideas about the supply side of the economy. In other words, they say the economy is growing slowly because we are running out of new inventions or natural resources. The secular stagnation hypothesis, by contrast, is the view that the economy can no longer be trusted to maintain an adequate level of demand. One way to dramatize the difference is to specifically focus on unemployment. The technological slowdown hypothesis is primarily the belief that we won’t get much richer over the next few years, even if people do manage to get jobs. The secular stagnation hypothesis is the opposite view — the view that we may get a bunch of shiny new gadgets, but unemployment will stay high.

So far it is hard to know if there has been a big sudden slowdown in productivity because productivity is badly measured, but there has clearly been a big spike in unemployment and a drop in interest rates and inflation despite dramatic expansions of the monetary base. There is simply much more evidence of a secular drop in aggregate demand than a drop in aggregate supply. It is hard to explain high unemployment, rising inequality, low inflation, and dropping gasoline & energy prices in a world with constrained supply. Tyler Cowen argues that secular stagnation requires high storage costs of capital, and that may be a feature of the new Egertsson and Mehrotra model of secular stagnation, but all you need for a shortfall of demand is an equilibrium where there is excessive hoarding of financial capital.

There is far too little effort to measure hoarding, but Paul Krugman recently showed a graph of hoarding in the corporate sector:

Profits are very high, so why are companies concluding that they should return cash to stockholders rather than use it to expand their businesses? After all, we normally think of high profits as a signal: a profitable business is one people should be trying to get into. But right now we see a combination of high profits and sluggish investment.

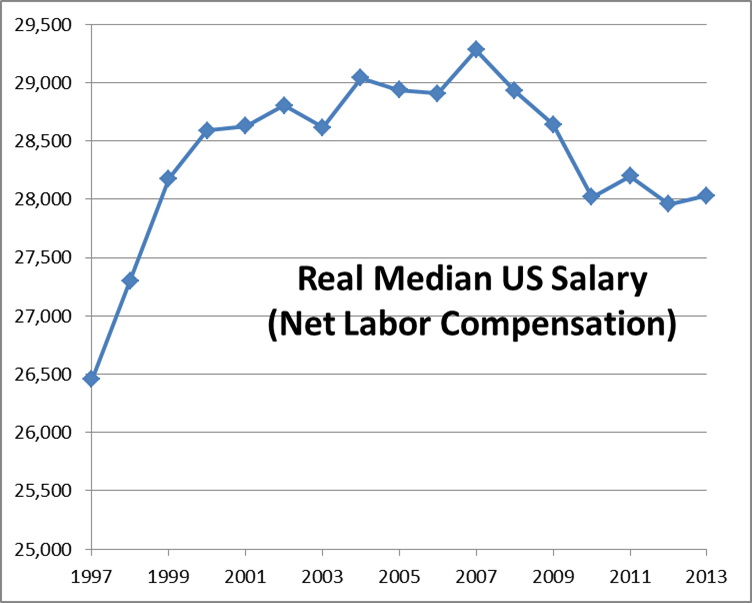

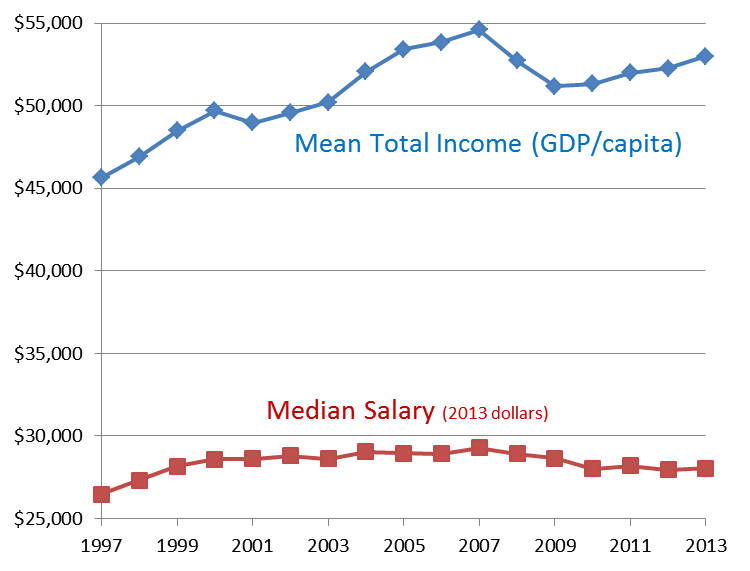

The profits are being paid to wealthy shareholders who don’t know what else to do with the money and it is being hoarded. If our corporations invested the money in capital and research (and increased the red line on the graph), that would help raise median salaries and productivity. Again, this graph does not look like a world with a supply (productivity) constraint. If there was a supply problem, profits would not be so high or there would be more incentive to invest. Plus, there would be less hoarding as wealthy people spend down their hoardings by buying whatever became limited in supply. Although a lot of people like Cowen suddenly perceived supply shortages during the financial crisis of 2007, it is hard to find any concrete examples. And why would a supply shortfall hurt the median American more than the elites?