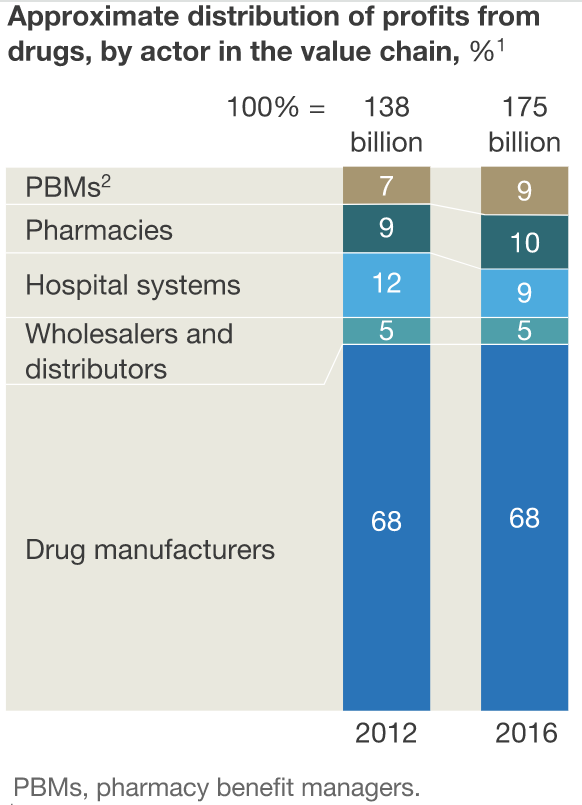

Most people have never heard of a Pharmacy Benefit Management company (PBM), but a PBM probably has tremendous control over the kinds of medicines you are prescribed and sets the prices you pay for them. It has been one of the fastest growing sectors in healthcare since 2000 and they are so new and so buried within our health administration bureaucracy that most people have no idea how important they have become. According to The Pharmacy Times, “the top 3 PBMs within the country manage the drug benefits for approximately 95% of the US population or 253 million American lives.” Mckinsey shows how fast PBMs grew over just four years and how they ate away at the revenues of hospitals as they reshaped the pharmaceutical marketplace:

PBMs and retail pharmacies captured a greater share of total profits from the pharmaceutical value chain in 2016 than in 2012… This increase came almost entirely at the expense of hospital systems’ share of profits from drugs; manufacturers were largely able to maintain their share. During this time, hospitals saw their margins from drug sales decline by almost 30%. Hospital spending on drugs grew by 7% to 11% per year, far outstripping growth in reimbursements from both commercial and government payers

PBMs are middlemen between the insurance companies (and sometimes individual patients) who pay for drugs, the medical practices who prescribe them, the pharmaceutical manufacturers who make them and the retail pharmacies that distribute the drugs to patients. PBMs make money in 3 main ways: 1) rebates; 2) administrative fees; and 3) pharmacy spread:

-

A rebate is a fee (or bribe if you are less charitable) that a pharmaceutical manufacturer pays a PBM for including a drug on an insurance plan or hospital formulary. This is a surprisingly big part of the industry:

Approximately one-third of the net price paid for prescription drugs is traceable to these rebates and, as a result, consumers may already be paying one-third more from rebates alone.6 In addition, patients are often forced to switch their drug therapy based upon these rebates that dictate the plan’s formulary regardless of their efficacy. If patients or their providers want the patient to stay on the original drug therapy, then they are forced to obtain a prior authorization before the PBM will authorize coverage for the drug product. This practice is alarming since a patient’s drug therapy may be interrupted as a result and can lead to patient harm.

- An administrative fee is charged to the insurance company or hospital for managing the plan’s formulary.

- The pharmacy spread is the gap between what the patient and/or insurance company pays for a drug and the price that the PBM has negotiated with a particular pharmacy.

PBMs are paid by insurance companies to negotiate for lower prices from pharmacies and select the most cost effective drugs for any particular treatment (the formulary). Most countries have national treatment guidelines and/or formulary manuals, but in the US there is no national best practice and formularies are fragmented: each hospital and/or insurance plan can have a different formulary. PBMs help them figure out what drugs are the most cost effective for treating different diseases which is also dependent upon how cheaply the PBM can get each drug by negotiating a bulk discount from pharmacies. PBMs generally create formularies with different tiers of pricing. For example, a formulary for an insurance company typically has drugs that are not covered at all, drugs that have higher percent of the cost paid by the insurer (typically generic drugs), and drugs for which the insurer pays a lower percentage to discourage their use.

PBMs also help hospitals create formularies and there are sometimes problems when patients are given one drug in the hospital as dictated by the hospital formulary and then have a different formulary for outpatient care and have to switch medications after discharge.

In addition to these problems, unfortunately, the business model of PBMs is badly aligned with the interests of society, so it is unlikely that they make the kind of rational cost-benefit analysis in selecting formularies and pricing that would lead to the healthiest population for the amount of spending that we do. For example, PBMs make money from insurance companies for saving them money on drugs, not for providing quality care and so PBMs are blamed for causing delays such as, “Nurses spend 16 hours on the phone, medications take months to arrive, and patients suffer as they wait.”

Their first and third sources of revenues listed above give them perverse incentives to put profits over patients. First, they take bribes from drug manufacturers to skew their formularies in favor of manufacturers who pay the biggest bribe rather than selecting the most cost effective drug. That should be illegal and if you want to argue (as in the Citizens United ruling) that corporations are people and money is their main form of speech which cannot be banned due to the constitutional right to freedom of speech, then at least they shouldn’t be doing it under the table. We deserve to at least know who is buying influence over us by “speaking” with cash and how big a part of the PBMs’ budget is coming from different manufacturers. The PBMs’ third revenue stream is having patients pay more for drugs than the price the PBM negotiated with the pharmacy. This gives the PBMs zero incentive to pass on lower prices to consumers. I have sometimes found that the regular retail price for people without insurance was lower than the “discount” price my insurance company’s PBM has negotiated. That either means that my company’s PBM is utterly incompetent at negotiating prices or else they are skimming a healthy profit by getting people like me to pay a higher that normal price from the pharmacy and getting a kickback. It is always worth checking both the regular retail price and your insurance company’s “discount” price when you buy drugs. Otherwise you won’t know how well your PBM is doing its job.

PBMs get discounted drugs because they have more negotiating power because they negotiate for millions of patients. If you try to negotiate a lower price as an individual, sellers will laugh at you because you have no negotiating clout. You are a price taker. But if you could band together with a million other patients in a kind of consumer’s union, you would have a lot of market power to demand lower prices for the group. PBMs buy more drugs than individual hospitals or even insurance plans, so they can negotiate cheaper prices. That is one way PBMs make money. In fact, PBMs are so anxious to get more patients in their network, some will let you join their discount plan for free. I actually tried this. I bought a vaccine last year with a free “discount drug card” that gave me a lower price than what I would have paid through my insurance (which uses some other PBM). Ironically those free PBM discount cards may have more incentive to lower prices than your insurance company’s PBM because if you get insurance from your employer, you are a captive customer whereas the PBMs that give out free cards at least face some competition and have to have some reputation for negotiating better prices or nobody will bother joining.

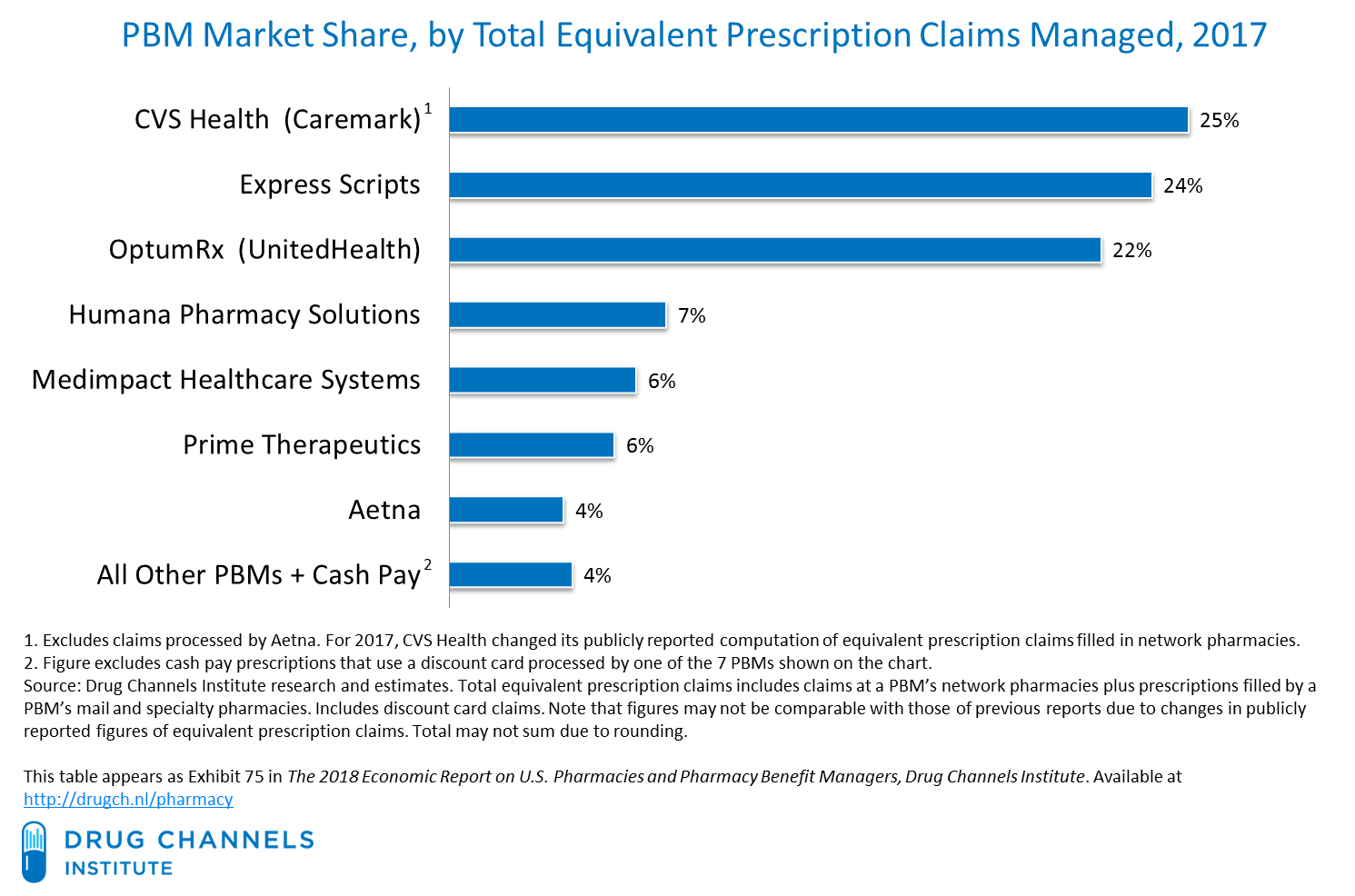

Because bigger PBMs have more negotiating power, smaller PBMs are at a disadvantage. That is why three PBMs already dominate the entire market. The top three companies already covered 75% to 80% of Americans in 2014. They represent three very different types of company according to Cole Werble at Health Affairs:

The current top-three firms represent three different models: the standalone PBM (Express Scripts); the PBM aligned with a major retail drugstore (CVS Health); and a PBM associated with a major health insurer (OptumRx, UnitedHealth Group).

Adam Fein has a graph showing the dominance of these top three companies:

At this point already, all the pharmacies other than CVS just have two big independent PBMs that they can work with and all the health insurers other than UnitedHealth also just have two big independent PBMs. I predict that Walgreens (the second largest pharmacy retailer after CVS mentioned above) will try to acquire PBM capacity too to cut out that middleman and Anthem (the second biggest health insurer after United Health mentioned above) will try to acquire with a PBM for the same reason. But Walmart (the third biggest pharmacy retailer) and even Amazon will probably be trying to squeeze the PBM industry too. Mckinsey predicts that the pharmaceutical market is ripe for disruption by online retail and Amazon will soon try to disrupt it:

At this point already, all the pharmacies other than CVS just have two big independent PBMs that they can work with and all the health insurers other than UnitedHealth also just have two big independent PBMs. I predict that Walgreens (the second largest pharmacy retailer after CVS mentioned above) will try to acquire PBM capacity too to cut out that middleman and Anthem (the second biggest health insurer after United Health mentioned above) will try to acquire with a PBM for the same reason. But Walmart (the third biggest pharmacy retailer) and even Amazon will probably be trying to squeeze the PBM industry too. Mckinsey predicts that the pharmaceutical market is ripe for disruption by online retail and Amazon will soon try to disrupt it:

The threat of technology-driven disruption of the pharmaceutical value chain is also becoming real. This threat made headlines with Amazon’s apparent intention to enter the market, as reflected in its hiring of pharmacy professionals in May 2017 and its acquisition of wholesale drug, medical device, and supply licenses in at least 12 states by October 2017.15 Retail pharmacies are already acutely aware of the potential of technology-driven disruption, as front-of-store pharmacy revenues have been virtually flat since 2012 due to the digital transformation of the retail industry. (The pharmacies have experienced revenue growth below 1% for general merchandise and 2% for over-the-counter medications; the comparable numbers in the overall US market are about 2% and 4%, respectively.16 ) Although the opportunities for Amazon or a similar technology entrant are significant, so are the challenges.

Several primary arguments underlie the belief that such a company could successfully disrupt the pharmaceutical value chain. First, the size and attractiveness of the market ($500 billion in revenues) could warrant aggressive investment. Indeed, pharmacy is the second-largest retail category in the United States and the only large category in which Amazon does not yet have a meaningful presence. Second, the economic spread across the value chain is large and could be ripe for potential disruption. Nearly $100 billion in gross margins are being retained by intermediaries across the pharmacy value chain. Finally, evidence exists that demand for direct purchasing of drugs online by consumers could be on the rise.

One of the big problems of the PBM industry is that they reduce price transparency. Each person buying drugs gets a different price depending on what their PBM has negotiated. That makes it difficult to comparison shop because there isn’t a single price that everyone pays. Each customer has to give their insurance card (or separate PBM discount card) to a pharmacist and ask for their customized price. Hopefully, the advent of online drug retailers of will reduce that problem by making prices easier to comparison shop.

Another barrier to comparison shopping that has arisen during in the PMB era is the decline of universally transferable prescriptions. In the twentieth century, doctors gave patients paper prescriptions that they could take anywhere which made it easy to comparison shop. Nowadays my doctors usually want to send a single electronic prescription to a single retailer which locks me in and makes it hard to comparison shop. If you find that your pharmacy has ridiculous prices you have to go back to your doctor and request another electronic prescription. It would be simple in the information age to have a transferable electronic prescription that worked better than the old paper system, but the people who have designed our electronic prescription system have made it more profitable for the pharmaceutical industry by reducing consumer power. Are PBMs partly to blame? Well they call themselves the managers of our pharmaceutical benefits and they took over this role shortly before the transition to the electronic system. If they wanted a better electronic system that gave consumers as much flexibility as the old system, they have a lot of behind-the-scenes power to manage how pharmaceuticals are sold.

This power has made them a lot of enemies. The drug manufacturers blame them for inflating drug costs and creating and “unfair”, “complex” and “opaque” system with “broken incentives”. The American Prospect magazine agrees and argues that hospitals and pharmaceutical retailers haven’t been able to do anything about the problem because PBMs have acquired so much monopoly power over the industry. For example, CVS is using the monopoly power of its enormous PBM to put small mom-and-pop pharmacies out of business and then they buy up the closing pharmacies for cheap. This is what happened to my local pharmacy in Bluffton Ohio last year. Health Affairs magazine also agrees about the evils of PBMs and Michael Carrier wrote an editorial there suggesting several possible ways the government could fix the system with regulatory changes.

[…] In most rich nations the government holds down pharmaceutical prices by negotiating with manufacturers for discounted prices. Although the US government (via Medicare, Medicaid, the VA, etc.) is by far the largest buyer of drugs in the world, it is also the only buyer in the world that cannot legally negotiate prices because the government has banned itself from doing so. So the government is stuck paying the highest price (the list price) along with unlucky individual Americans who have a bad PBM. […]